本文介绍了机器学习中的基本概念,包括训练样例的表示、预测函数和损失函数的定义,以及梯度下降法和正规方程法这两种优化策略。通过实例展示了如何在MATLAB中实现数据预处理、损失函数计算和梯度下降法更新参数的过程,同时也探讨了两种优化方法的对比和应用。

本文介绍了机器学习中的基本概念,包括训练样例的表示、预测函数和损失函数的定义,以及梯度下降法和正规方程法这两种优化策略。通过实例展示了如何在MATLAB中实现数据预处理、损失函数计算和梯度下降法更新参数的过程,同时也探讨了两种优化方法的对比和应用。

对数据表示做一些规定

x j ( i ) = v a l u e o f f e a t u r e j i n t h e i t h t r a i n i n g e x a m p l e x i = t h e i n p u t ( f e a t u r e ) o f t h e i t h t r a i n i n g e x a m p l e m = t h e n u m b e r o f t r a i n i n g e x a m p l e s n = t h e n u m b e r o f f e a t u r e s x_j^{(i)} = value\ of\ feature\ j\ in\ the\ i^{th}\ training\ example \\ x^{i} = the\ input\ (feature)\ of\ the\ i^{th}\ training\ example \\ m = the\ number\ of\ training\ examples \\ n = the\ number\ of\ features \\ xj(i)=value of feature j in the ith training examplexi=the input (feature) of the ith training examplem=the number of training examplesn=the number of features

预测函数,损失函数表示

h

y

p

o

t

h

e

s

i

s

f

u

n

c

t

i

o

n

:

h

θ

(

x

)

=

θ

0

+

θ

1

x

1

+

θ

2

x

2

+

⋯

+

θ

n

x

n

hypothesis \ function:\ h_{\theta}(x) = \theta_0+ \theta_1x_1+ \theta_2x_2+\cdots+ \theta_nx_n

hypothesis function: hθ(x)=θ0+θ1x1+θ2x2+⋯+θnxn

c

o

s

t

f

u

n

c

t

i

o

n

:

J

(

θ

)

=

1

2

m

∑

i

=

1

m

(

h

θ

(

x

i

)

−

y

i

)

2

cost \ function: \ J(\theta) = \frac{1}{2m}\sum\limits_{i=1}^{m}(h_\theta(x_i)-y_i)^2

cost function: J(θ)=2m1i=1∑m(hθ(xi)−yi)2

梯度下降法

repeat until convergence:{

θ

j

=

θ

j

−

α

∂

J

(

θ

)

∂

θ

j

=

θ

j

−

α

1

m

∑

i

=

1

m

(

(

h

θ

(

x

(

i

)

)

−

y

(

i

)

)

x

j

(

i

)

)

\\ \theta_j = \theta_j - \alpha\frac{\partial J(\theta)}{\partial\theta_j} = \theta_j - \alpha\frac{1}{m}\sum\limits_{i=1}^{m}((h_\theta(x^{(i)}) - y^{(i)})x_j^{(i)})

θj=θj−α∂θj∂J(θ)=θj−αm1i=1∑m((hθ(x(i))−y(i))xj(i))

}

数据归一化

x − μ σ \frac{x-\mu}{\sigma} σx−μ

正规方程法

θ = ( X T X ) − 1 X T y \theta = (X^TX)^{-1}X^Ty θ=(XTX)−1XTy

梯度下降法和正规方程法对比

matlab下演练

假设有数据特征矩阵X为47 × \times × 2表示47个样本,2个特征。同时y表示结果矩阵,大小为为47 × \times × 1。 θ \theta θ 初始化为47 × \times × 1的全零向量。

- 首先,一般会为其增加全1列(即

h

(

θ

)

=

w

0

+

x

1

w

1

+

x

2

w

2

h(\theta) = w_0+x_1w_1+x_2w_2

h(θ)=w0+x1w1+x2w2 一般为

w

0

w_0

w0 补充

x

0

x_0

x0 为1)

X = [ones(m, 1) X]; - 归一化

mu = mean(X);

sigma = std(X);

X_norm = (X - mu)./sigma; - 计算损失函数

J = sum((X* theta - y).^2)/(2*m); - 梯度下降

for iter = 1:num_iters:

theta = theta - alpha * (X’((Xtheta) - y)) / m;

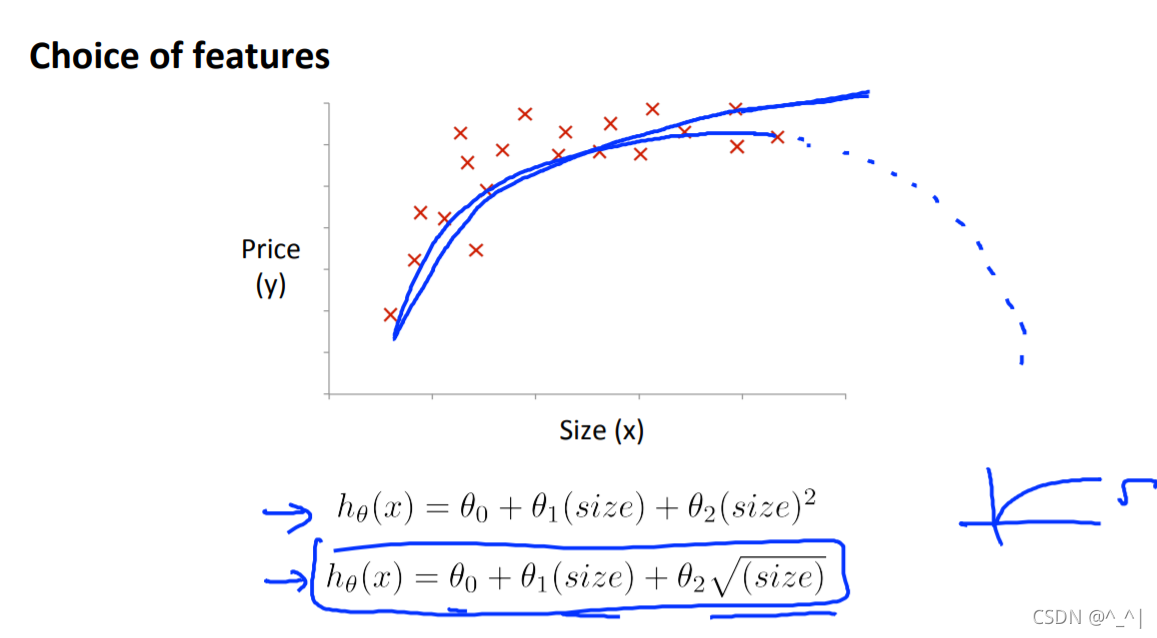

非线性化

258

258

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言