本文详细介绍了如何通过移动平均和标准差图检测时间序列的平稳性,使用ADF检验验证单位根假设,然后通过一阶12步差分处理非平稳序列,并对差分后的序列进行白噪声检验。通过ACF和Q统计量的分析,确认数据是否符合白噪声特征,以支持后续的经济预测建模。

本文详细介绍了如何通过移动平均和标准差图检测时间序列的平稳性,使用ADF检验验证单位根假设,然后通过一阶12步差分处理非平稳序列,并对差分后的序列进行白噪声检验。通过ACF和Q统计量的分析,确认数据是否符合白噪声特征,以支持后续的经济预测建模。

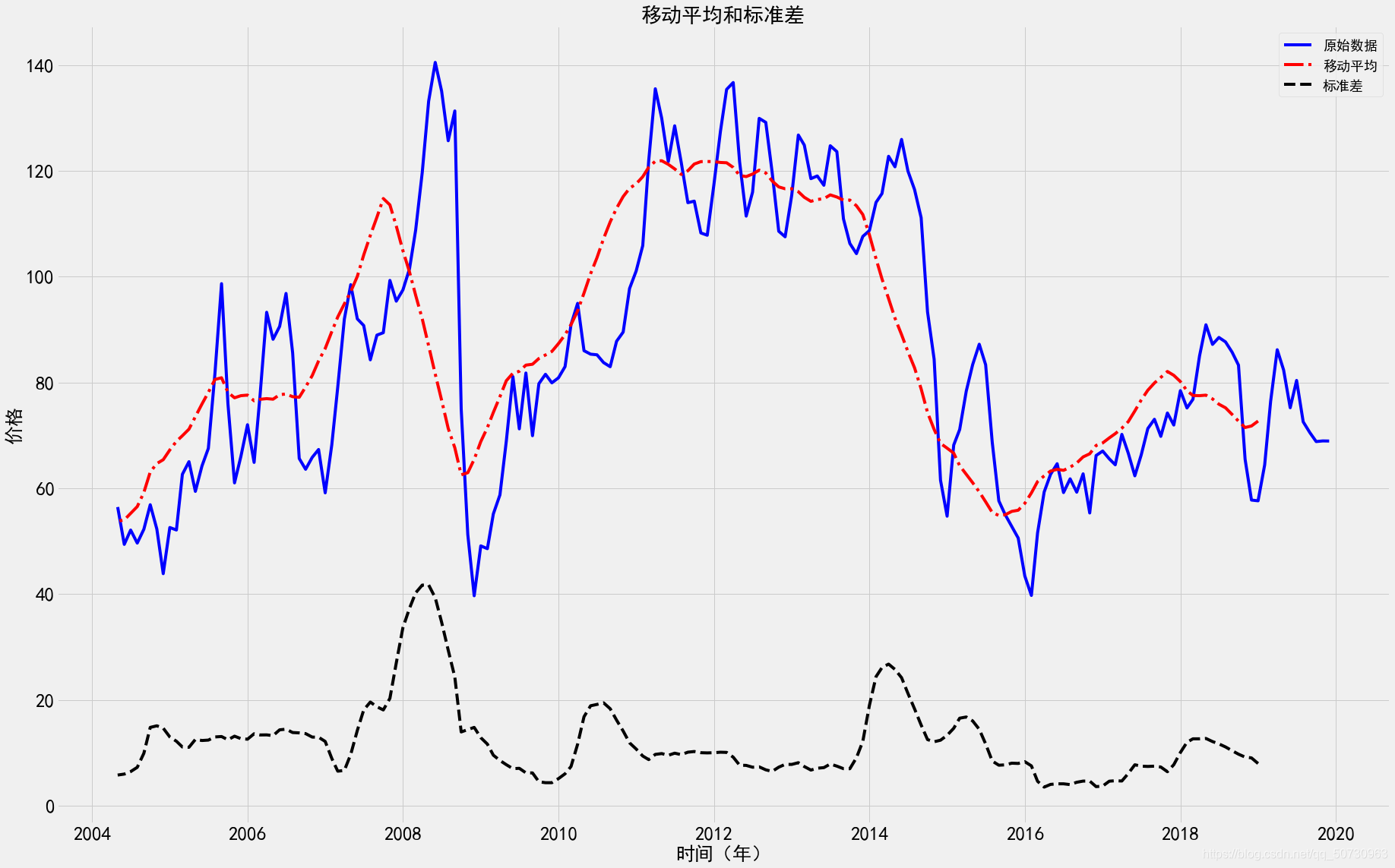

四、绘制移动平均值和标准差

定义函数TestStationaryPlot来检验序列的平稳性。

def TestStationaryPlot(ts):

rol_mean = ts.rolling(window = 12, center = False).mean()

rol_std = ts.rolling(window = 12, center = False).std()

plt.plot(ts, color = 'blue',label = u'原始数据')

plt.plot(rol_mean, color = 'red', linestyle='-.', label = u'移动平均')

plt.plot(rol_std, color ='black', linestyle='--', label = u'标准差')

plt.xticks(fontsize = 25)

plt.yticks(fontsize = 25)

plt.xlabel(u'时间(年)', fontsize = 25)

plt.ylabel(u'价格', fontsize = 25)

plt.legend(loc='best', fontsize = 18)

plt.title(u'移动平均和标准差', fontsize = 27)

plt.show(block= True)

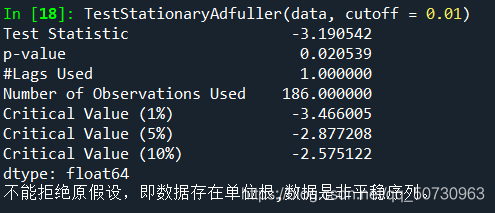

五、ADF检验

定义TestStationaryAdfuller函数,对序列进行ADF检验。

def TestStationaryAdfuller(ts, cutoff = 0.01):

ts_test = adfuller(ts, autolag = 'AIC')

ts_test_output = pd.Series(ts_test[0:4], index=['Test Statistic','p-value','#Lags Used','Number of Observations Used'])

for key,value in ts_test[4].items():

ts_test_output['Critical Value (%s)'%key] = value

print(ts_test_output)

if ts_test[1] <= cutoff:

print(u"拒绝原假设,即数据没有单位根,序列是平稳的。")

else:

print(u"不能拒绝原假设,即数据存在单位根,数据是非平稳序列。")结果为:

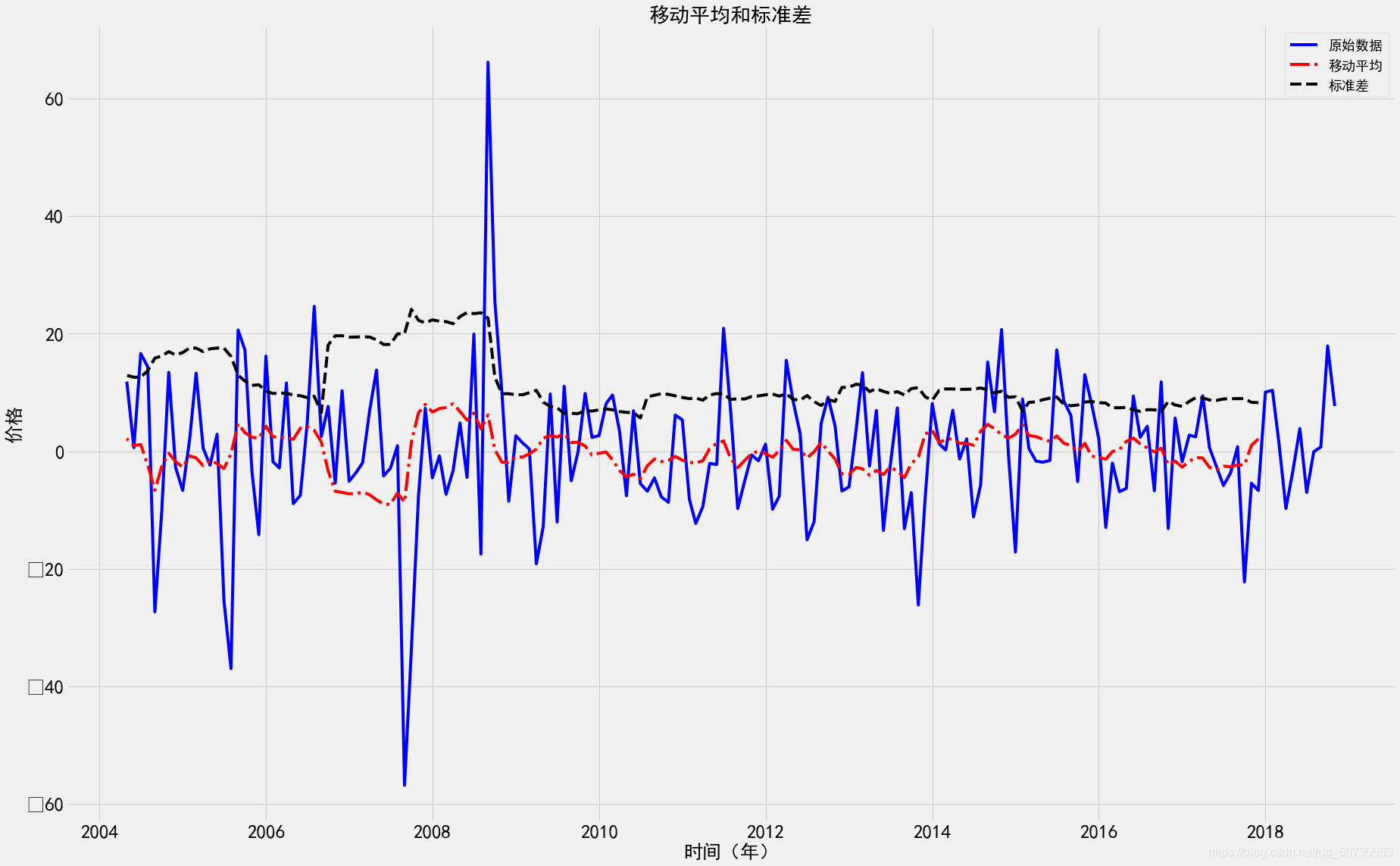

六、序列平稳化

对原始的序列作1阶12步差分来提取原序列的趋势效应和季节效应

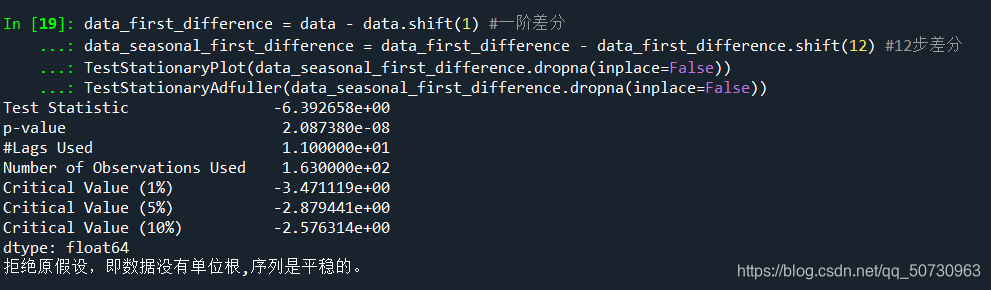

data_first_difference = data - data.shift(1) #一阶差分

data_seasonal_first_difference = data_first_difference - data_first_difference.shift(12) #12步差分

TestStationaryPlot(data_seasonal_first_difference.dropna(inplace=False))

TestStationaryAdfuller(data_seasonal_first_difference.dropna(inplace=False))

差分后的序列图及检验结果如下

七、白噪声检验

#白噪声检验

data_seasonal_first_difference.dropna(inplace = True)

r,q,p = sm.tsa.acf(data_seasonal_first_difference.values.squeeze(), qstat=True)

data = np.c_[range(1,41), r[1:], q, p]

table = pd.DataFrame(data, columns=['lag', "AC", "Q", "Prob(>Q)"])

print(table.set_index('lag'))

AC Q Prob(>Q)

lag

1.0 0.134548 3.222653 0.072626

2.0 -0.057476 3.814125 0.148516

3.0 -0.084782 5.108603 0.164015

4.0 0.020234 5.182766 0.269053

5.0 -0.030606 5.353444 0.374284

6.0 -0.050748 5.825469 0.443023

7.0 -0.036542 6.071665 0.531407

8.0 -0.088600 7.527678 0.480911

9.0 0.024161 7.636606 0.571141

10.0 0.060250 8.318058 0.597800

11.0 0.021679 8.406821 0.676464

12.0 -0.451548 47.153245 0.000004

13.0 -0.141176 50.964087 0.000002

14.0 -0.032962 51.173120 0.000004

15.0 0.032890 51.382538 0.000007

16.0 0.088978 52.924864 0.000008

17.0 0.026148 53.058906 0.000014

18.0 0.068606 53.987511 0.000018

19.0 0.067750 54.898894 0.000024

20.0 -0.008665 54.913899 0.000042

21.0 0.051037 55.437822 0.000061

22.0 -0.050116 55.946305 0.000087

23.0 -0.068516 56.902939 0.000106

24.0 -0.114977 59.614739 0.000072

25.0 0.077896 60.867741 0.000079

26.0 0.092983 62.665093 0.000073

27.0 0.021314 62.760171 0.000113

28.0 -0.083681 64.235713 0.000114

29.0 0.011723 64.264871 0.000177

30.0 -0.011195 64.291645 0.000270

31.0 -0.077984 65.599812 0.000281

32.0 0.028559 65.776476 0.000401

33.0 -0.003386 65.778978 0.000594

34.0 0.110049 68.439499 0.000419

35.0 -0.004910 68.444834 0.000614

36.0 0.100167 70.680700 0.000488

37.0 -0.044029 71.115823 0.000628

38.0 -0.082991 72.673049 0.000598

39.0 -0.016350 72.733935 0.000840

40.0 0.021184 72.836899 0.001153

白噪声检验结果可知,1阶12步差分后的序列延迟1-12期时,Q统计量的P值均小于0.01,所以在0.01的显著性水平下,拒绝原假设,即1阶12步差分后的序列是非白噪声序列

1万+

1万+

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言