使用隐马尔科夫模型分析基金净值数据,预测基金走势。模型通过基金历史净值变化率训练,生成未来净值趋势,适用于如沪深300指数基金等时间序列数据预测。

使用隐马尔科夫模型分析基金净值数据,预测基金走势。模型通过基金历史净值变化率训练,生成未来净值趋势,适用于如沪深300指数基金等时间序列数据预测。

隐马尔可夫模型是生成模型,可用于分析股票、基金这样的时间序列数据。

用隐马尔科夫模型来预测基金数据。基金净值数据是典型的时间序列数据示例,其数据都是用日期格式来组织的。

cd \Anaconda3\Scripts

pip install hmmlearn

hmm_fund.py

# coding: utf-8

import os, sys

import datetime

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

from hmmlearn.hmm import GaussianHMM

if len(sys.argv) ==2:

code = sys.argv[1]

else:

print('usage: python hmm_fund.py fundcode ')

sys.exit(1)

if len(code) !=6:

print('fund code length: 6')

sys.exit(2)

f1 = code+'.csv'

if not os.path.exists(f1):

print(f1 +' is not exists. ')

sys.exit(3)

df = pd.read_csv(f1, index_col='date')

if len(df) <100:

print(" len(df) <100 ")

sys.exit(2)

# 基金净值

net_values = np.array(df['jz'].values)

# Take diff of net values and computing rate of change

diff_percentage = 100.0 * np.diff(net_values) / net_values[:-1]

# Stack the percentage diff and net values column-wise for training

X = np.column_stack([net_values[1:], diff_percentage])

print(X[-5:])

print('percent_sum:',X[:,1].sum())

# Create and train Gaussian HMM

print(" Training HMM....")

model = GaussianHMM(n_components=5, covariance_type="diag", n_iter=1000)

model.fit(X)

# Generate data using model

num_samples = 500

samples, _ = model.sample(num_samples)

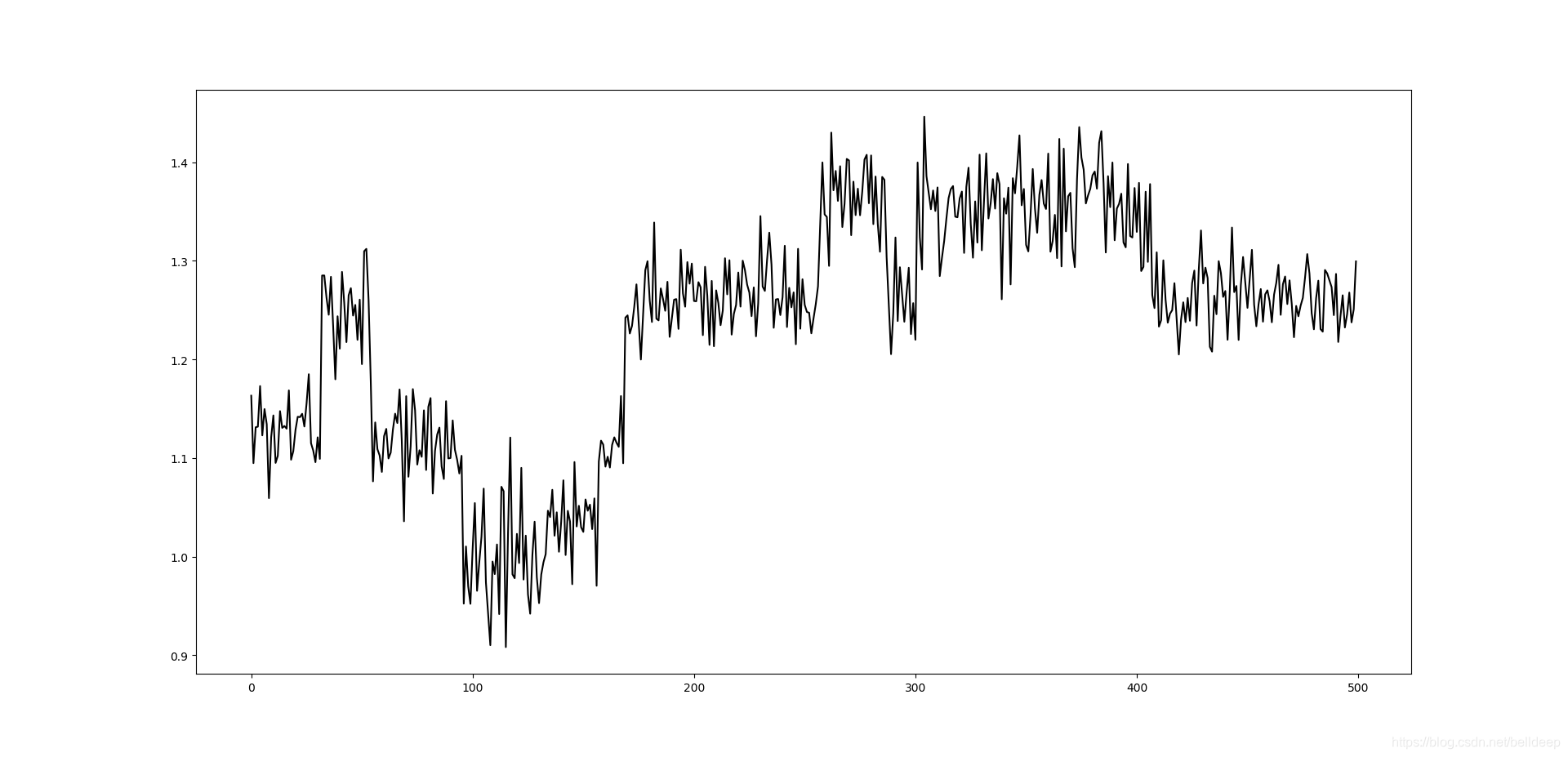

plt.plot(np.arange(num_samples), samples[:,0], c='black')

plt.title(code)

plt.grid()

plt.show()

基金净值数据格式:

date,jz,ljjz

2016-01-04,1.1141,1.1141

2016-01-05,1.1161,1.1161

2016-01-06,1.1350,1.1350

运行 python hmm_fund.py 660008

预测 forecast :660008 沪深300指数基金,2020年上半年基金净值在1.44~1.28元之间震荡,年中会有10%下跌,在下半年基金净值在1.33~1.21元之间波动。

参考书:[ Python机器学习经典实例 ] 第8章 解剖时间序列和时序数据

用隐马尔科夫模型分析股票市场数据 hmm_stock.py

年中会有10%下跌,

2020.7.10日预测:上证指数 3450 x 0.9 = 3105 点,沪深300指数基金 1.6768 x 0.9 = 1.5091

以上仅供学习编程参考,不可作为你的股市操作依据。

1763

1763

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言