本文详细介绍了风险管理与金融机构的第2章——银行,涵盖了商业银行、资本要求、存款保险、投资银行、证券交易等方面。讨论了银行面临的信用、市场和操作风险,并指出资本充足性、存款保险和投资银行业务(如IPO、荷兰式拍卖)在现代银行业中的作用。此外,还提及了银行潜在的利益冲突、会计审计和发起与配售模型。

本文详细介绍了风险管理与金融机构的第2章——银行,涵盖了商业银行、资本要求、存款保险、投资银行、证券交易等方面。讨论了银行面临的信用、市场和操作风险,并指出资本充足性、存款保险和投资银行业务(如IPO、荷兰式拍卖)在现代银行业中的作用。此外,还提及了银行潜在的利益冲突、会计审计和发起与配售模型。

typora-copy-images-to: Risk Management and Financial Institution

文章目录

- Risk Management and Financial Institution Chapter 2 —— Banks

Risk Management and Financial Institution Chapter 2 —— Banks

- Today, most large banks engage in both commercial and investment banking

- 商业银行做存贷业务,投行做发行股票、举债、并购重组、证券经纪等等业务

- 商业银行分为零售与整售,retail and wholesale,零售的存贷价差要高于整售,但整售的成本以及预期损失更低,整售的资金经常从货币中央银行借出,money center banks

2.1 Commercial Banking

-

监管事务包括:capital that banks must keep, the activities they are allowed to engage in, deposit insurance, and the extent to which mergers and foreign ownership are allowed

-

The structure of banking in the United States is largely a result of regulatory restrictions on interstate banking,架构源于美国监管条约中的跨州经营规定

-

两个阻力和弊端:

- 小银行失去市场份额

- 支票清算及其他付款服务会降低货币中心银行的盈利

-

McFadden Act 一个州之内只能开一家分行

-

成立多银行控股可以绕过法案

-

1970年限制令开始消失,互惠条约,reciprocal agreements

-

2010年颁布了Dodd-Frank Wall Street Reform and Consumer Protection Act

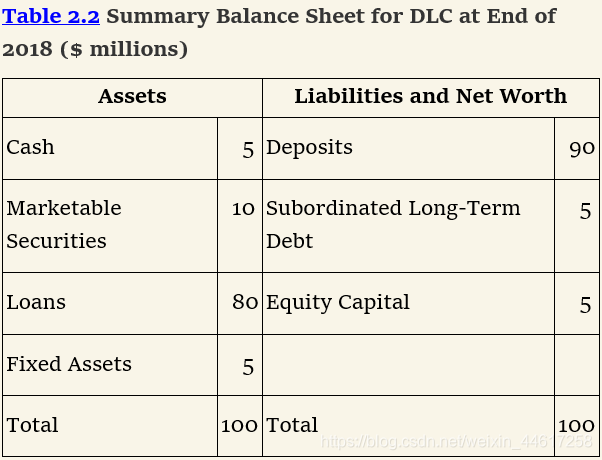

2.2 Capital Requirements of a small Commercial Bank

-

subordinated long‐term debt——bonds issued by the bank to investors that rank below deposits in the event of a liquidation 破产优先级仅次于存款

-

The equity capital consists of the original cash investment of the shareholders and earnings retained in the bank 股权资本由留存收益与最初投资组成

-

It is important for the bank to be managed so that net interest income remains roughly constant regardless of movements in interest rates of different maturities 不同利率环境下平缓利差收入至关重要

-

default 无法避免,导致 loan losses,违约率随着经济状况波动

最低0.47元/天 解锁文章

最低0.47元/天 解锁文章

6003

6003

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言