本文详细解析了吴恩达机器学习课程中的单变量线性回归实战案例,使用Python实现并详细解释了从数据导入、散点图绘制、代价函数计算、梯度下降法优化到模型预测的全过程。

本文详细解析了吴恩达机器学习课程中的单变量线性回归实战案例,使用Python实现并详细解释了从数据导入、散点图绘制、代价函数计算、梯度下降法优化到模型预测的全过程。

1. 单变量线性回归

网上有机器学习系列课程的很多资料,但是作业代码没有详细的解释。所以本博客给出了吴恩达机器学习作业的python实现,并且对基础知识进行详细的解释

首先引入需要用到的三个包

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

这三个包分别作用是线性代数 数据处理 画图。 pandas 是基于NumPy 的一种工具,该工具是为了解决数据分析任务

data = pd.read_csv('ex1data1.txt', header=None, names=['Population', 'Profit'])

#head()可以看一下前五行的数据。

# names把data里面的数据起了名字,以后可以使用这两个名字取数据了

data.head()

| Population | Profit | |

|---|---|---|

| 0 | 6.1101 | 17.5920 |

| 1 | 5.5277 | 9.1302 |

| 2 | 8.5186 | 13.6620 |

| 3 | 7.0032 | 11.8540 |

| 4 | 5.8598 | 6.8233 |

pd.read_csv把数据读取为DataFrame类型.数据中第一列是输入,第二是输出 这个数据是没有头的,所以header是空。

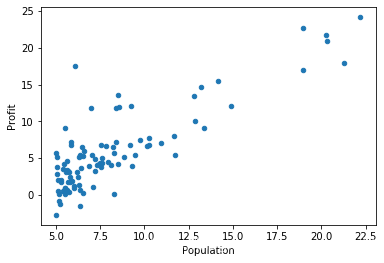

把数据用散点图画出来看一看,kind是scatter就是散点图:

data.plot(kind='scatter', x='Population', y='Profit')

plt.show()

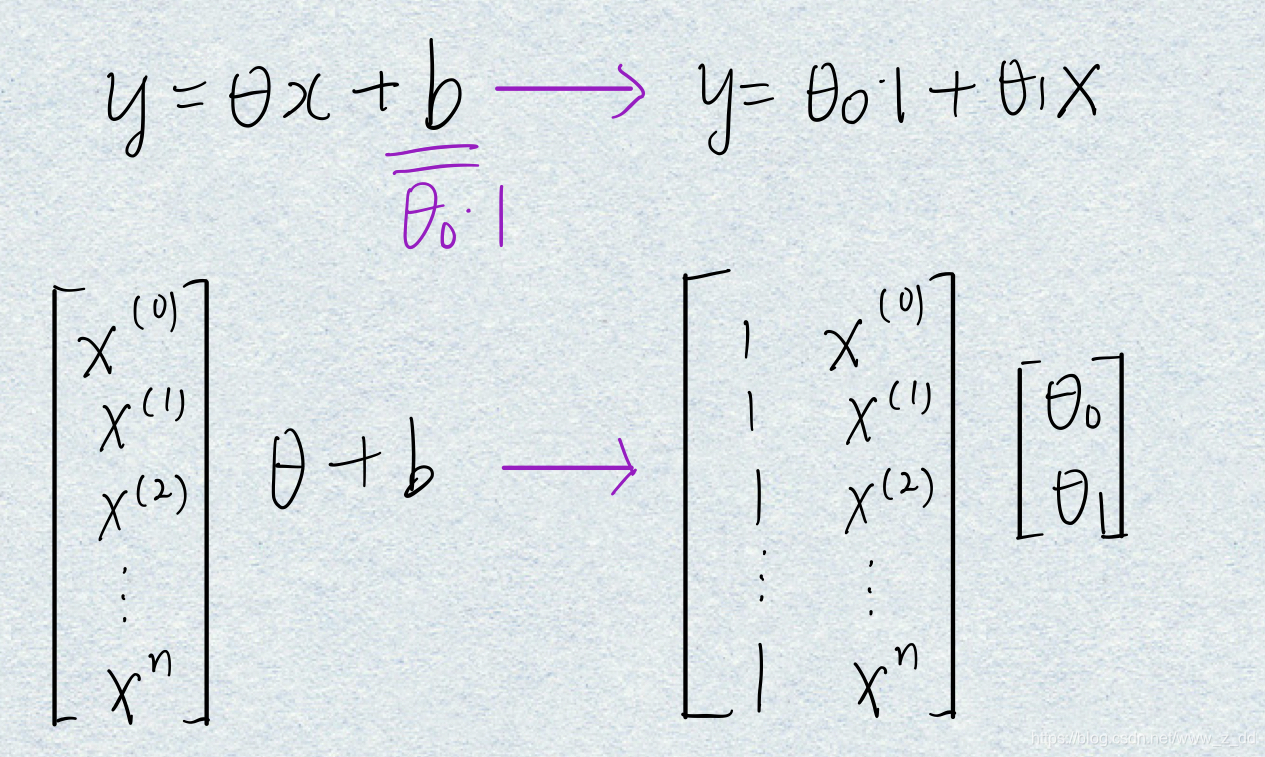

在X第一列插入一列,名字是ones,数据全是1

#如果使用iloc只选择了单独的一行会返回 Series 类型

#如果选择了多行数据则会返回 DataFrame 类型,

data.insert(0, 'Ones', 1)

y = data.iloc[:,2:3]与y = data.iloc[:,2]得到的也是不一样的类型

为什么要在X前面加1:

b是偏置,如果不加偏置b,建立的模型就只是经过原点的直线、平面等。

把截距b和斜率theta统一到一个框架下,就可以通过调整theta0来调整偏置b。

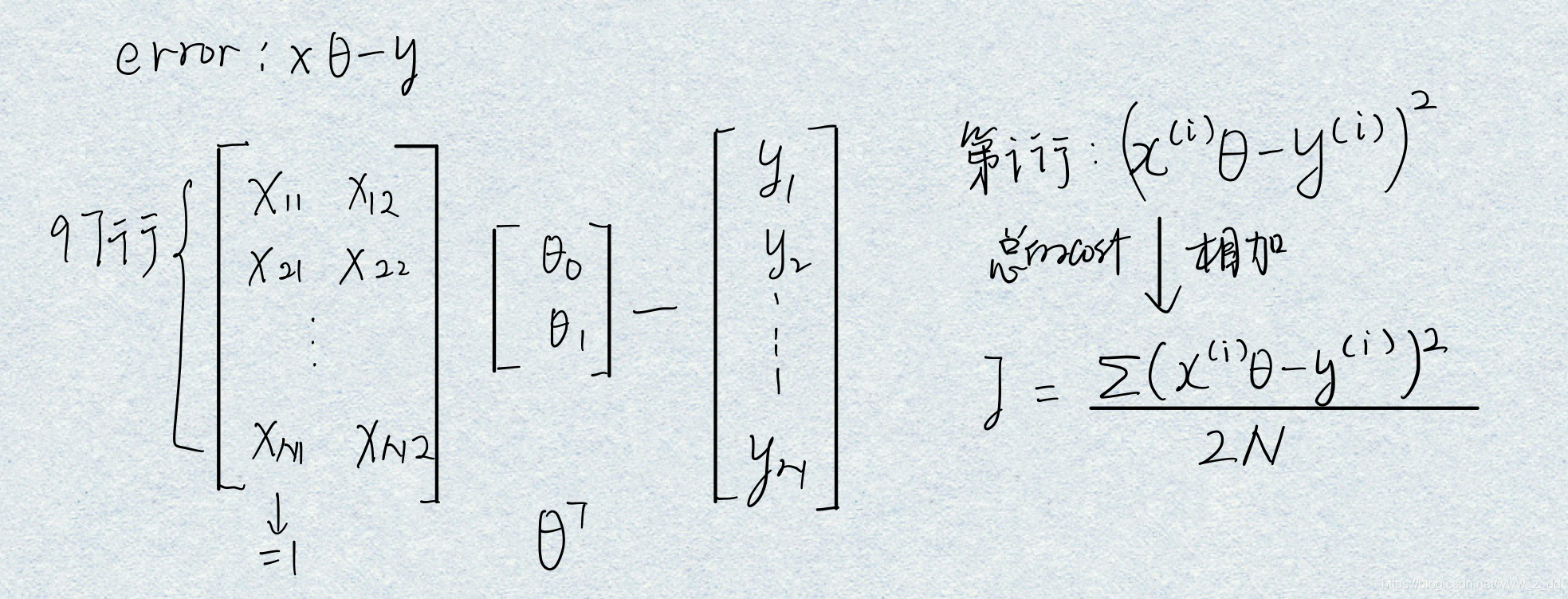

根据代价函数算出当前的参数也就是theta的误差;

编写代价函数。

def computeCost(X, y, theta):

inner = np.power(((X * theta.T) - y), 2) #对第一个参数平方

return np.sum(inner) / (2 * len(X)) #把矩阵的每一个元素加起来

计算一下初始的cost,也就是theta都为0的时候

computeCost(X, y, theta)

32.072733877455676

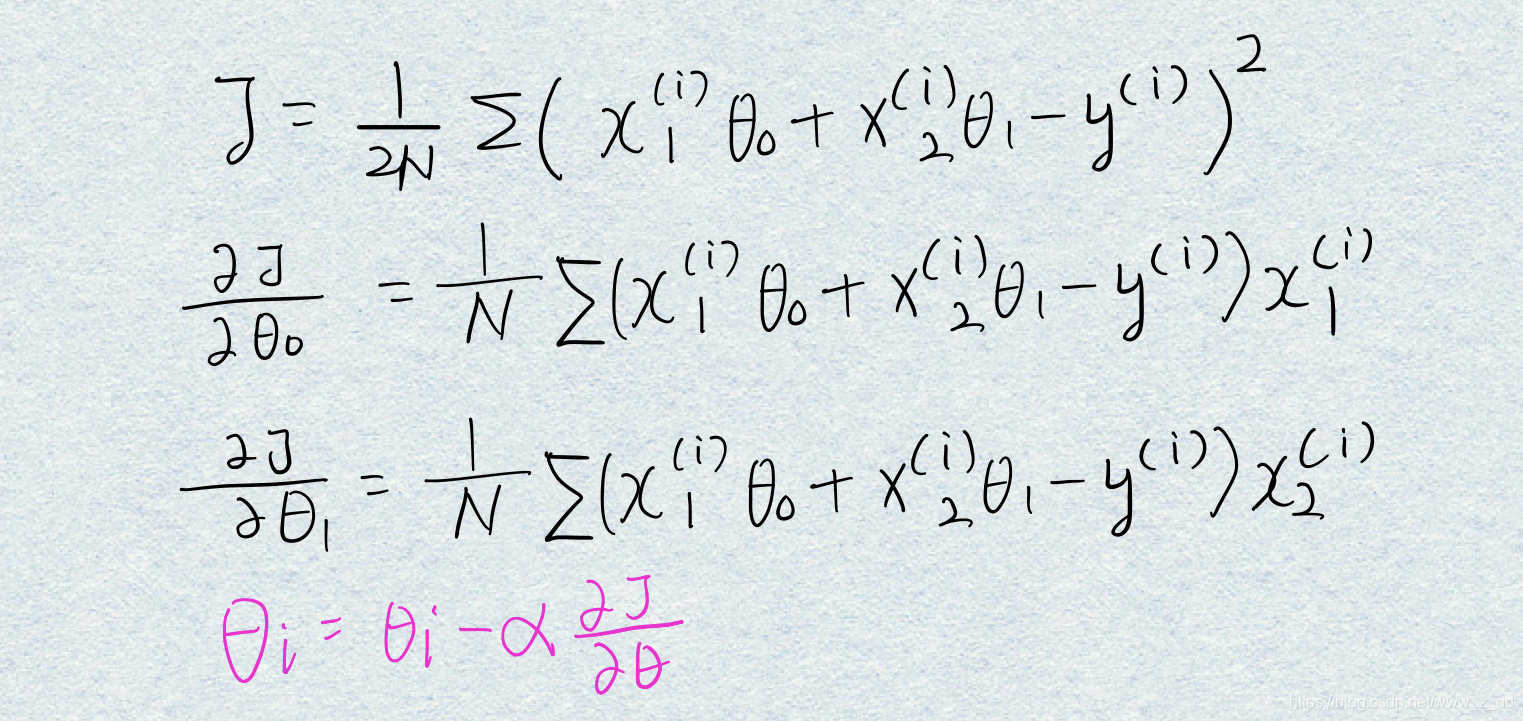

然后使用梯度下降法优化参数,也就是找到使代价函数最小的theta。

所以现在要求出梯度,对两个参数求导;然后迭代更新theta:

def gradientDescent(X, y, theta, alpha, iters):

temp = np.matrix(np.zeros(theta.shape))

parameters = int(theta.ravel().shape[1])

cost = np.zeros(iters) #保存每一次迭代的cost

for i in range(iters):

error = (X * theta.T) - y

for j in range(parameters): #一共有两列,对这两个参数更新

# np.multiply(error, X[:,j]) #两个N*1的矩阵对应的点相乘

temp[0,j] = theta[0,j] - ((alpha / len(X)) * np.sum( np.multiply(error, X[:,j])))

theta=temp

cost[i] = computeCost(X, y, theta)

return theta, cost

g, cost = gradientDescent(X, y, theta, 0.01, 1000)

computeCost(X, y, g)

4.515955503078912

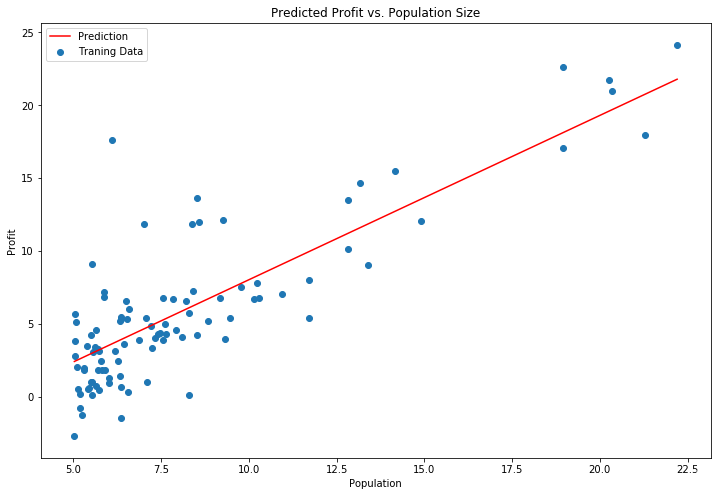

绘制刚刚建立的模型,就是一条直线

x = np.linspace(data.Population.min(), data.Population.max(), 100)

f = g[0, 0] + (g[0, 1] * x)

#把函数F画出来

fig, ax = plt.subplots(figsize=(12,8))

ax.plot(x, f, 'r', label='Prediction')

ax.scatter(data.Population, data.Profit, label='Traning Data')

ax.legend(loc=2)

ax.set_xlabel('Population')

ax.set_ylabel('Profit')

ax.set_title('Predicted Profit vs. Population Size')

plt.show()

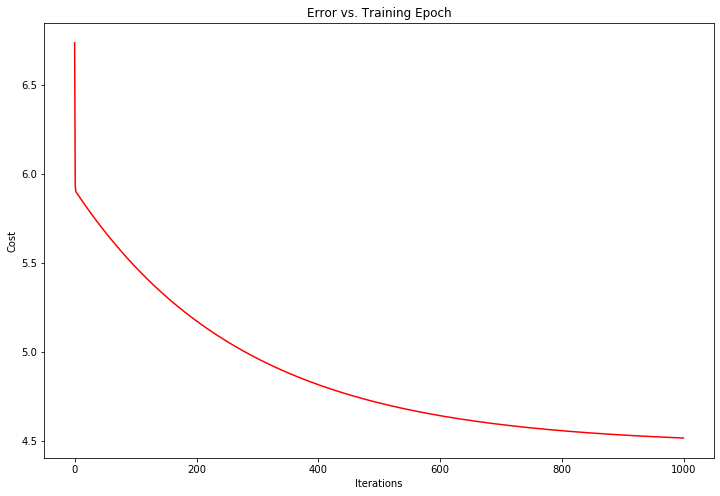

fig, ax = plt.subplots(figsize=(12,8))

ax.plot(np.arange(1000), cost, 'r')

ax.set_xlabel('Iterations')

ax.set_ylabel('Cost')

ax.set_title('Error vs. Training Epoch')

plt.show()

#随着迭代次数的增加,cost越来越小

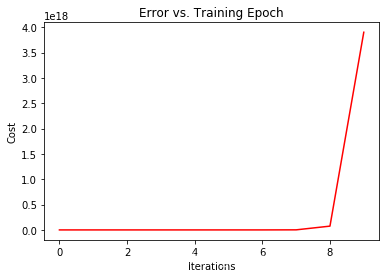

改变learning rate的值看一下

theta = np.matrix(np.array([0,0]))

g, cost = gradientDescent(X, y, theta, 0.1, 10)

fig, ax = plt.subplots(figsize=(6,4))

ax.plot(np.arange(10), cost, 'r')

ax.set_xlabel('Iterations')

ax.set_ylabel('Cost')

ax.set_title('Error vs. Training Epoch')

plt.show()

#随着迭代次数的增加,cost越来越小

二

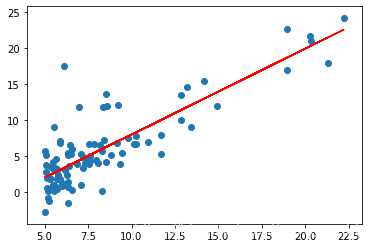

使用scikit-learn的线性回归函数,而不是从头开始实现这些算法。

from sklearn import linear_model

model = linear_model.LinearRegression()

model.fit(X, y)

x = np.array(X[:, 1].A1)

f = model.predict(X).flatten()

fig, ax = plt.subplots(figsize=(6,4))

ax.plot(x, f, 'r', label='Prediction')

#绘制模型

ax.scatter(data.Population, data.Profit, label='Traning Data')

#绘制数据的散点图

plt.show()

三

正规方程求解

只适用于线性模型,如果特征数量n较大则运算代价大,因为矩阵逆的计算时间复杂度为 𝑂(𝑛3) ,通常来说当 𝑛 小于10000 时还是可以接受的。

final_theta2=np.linalg.inv(X.T@X)@X.T@y

final_theta2

matrix([[-3.89578088],

[ 1.19303364]])

`

604

604

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言