本文详细介绍了线性回归模型在房价预测和股市预测中的应用,涉及模型假设(一元/多元线性)、损失函数的选择与梯度下降优化,以及如何通过训练集和测试集验证模型性能。讨论了过拟合问题、模型复杂度提升和正则化的应对策略。

本文详细介绍了线性回归模型在房价预测和股市预测中的应用,涉及模型假设(一元/多元线性)、损失函数的选择与梯度下降优化,以及如何通过训练集和测试集验证模型性能。讨论了过拟合问题、模型复杂度提升和正则化的应对策略。

一、定义

Regression就是找到一个函数function,通过输入特征x,得到一个返回值。

二、应用

- 房价预测

- 输入:根据房屋面积,地理位置等

- 输出:预测房屋的价格

- 股市的预测:

- 输入:过去10年股票的变动,新闻咨询,公司并购咨询等

- 输出:预测股市的明天的平均值

三、步骤

1、模型假设(线性模型)

一元线性模型

一元线性模型针对于单个输入特征的情况。以一个特征Xcp为例,此线性模型假设为: y = b + w x \mathrm{y}=\mathrm{b}+ \mathrm{w} \mathrm{x} y=b+wx

多元线性模型

在实际生活中,为得到所预测的返回值,往往输入的特征值Xcp不止一个。例如预测房价时,为得到此时房价,我们要考虑到房屋面积,地理位置等因素,特征值往往会很多。

所以㧴们假设 线性模型 Linear model:

y

=

b

+

∑

w

i

x

i

\mathrm{y}=\mathrm{b}+\sum \mathrm{w}_{\mathrm{i}} \mathrm{x}_{\mathrm{i}}

y=b+∑wixi

- x i \mathrm{x}_{\mathrm{i}} xi : 就是各种特征(feture)

- w i \mathrm{w}_{\mathrm{i}} wi : 各个特征的权重

- b: 偏移量

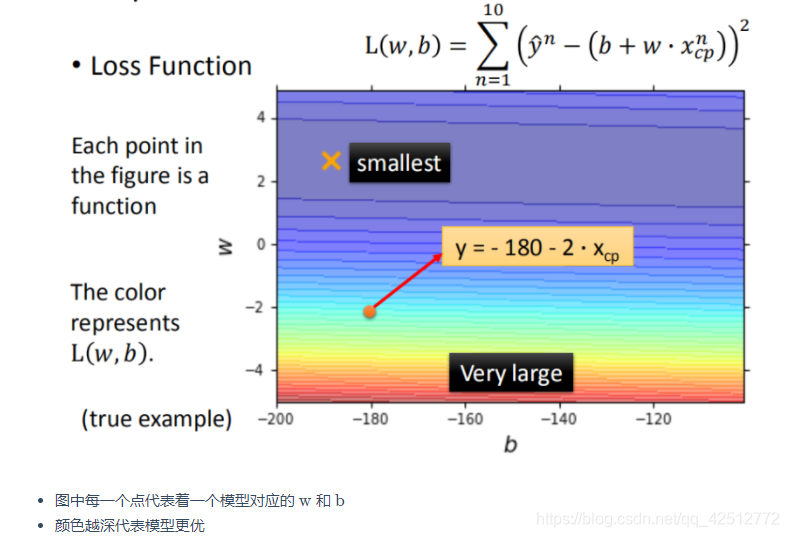

2、模型评估(损失函数)

求取理论值与预测值之间的差值,来判断所找寻的模型的好坏。即引入损失函数(Loss Function),用以衡量模型的好坏。定义损失函数为:

L

(

w

,

b

)

=

∑

n

=

1

10

(

y

^

n

−

(

b

+

w

⋅

x

c

p

)

)

2

\mathrm{L}(\mathrm{w}, \mathrm{b})=\sum_{\mathrm{n}=1}^{10}\left(\hat{\mathrm{y}}^{\mathrm{n}}-\left(\mathrm{b}+\mathrm{w} \cdot \mathrm{x}_{\mathrm{cp}}\right)\right)^{2}

L(w,b)=n=1∑10(y^n−(b+w⋅xcp))2

3、模型优化(梯度下降)

针对损失函数,

L

(

w

,

b

)

=

∑

n

=

1

10

(

y

^

n

−

(

b

+

w

⋅

x

c

p

)

)

2

\mathrm{L}(\mathrm{w}, \mathrm{b})=\sum_{\mathrm{n}=1}^{10}\left(\hat{\mathrm{y}}^{\mathrm{n}}-\left(\mathrm{b}+\mathrm{w} \cdot \mathrm{x}_{\mathrm{cp}}\right)\right)^{2}

L(w,b)=n=1∑10(y^n−(b+w⋅xcp))2

需要找到一个零结果最小的

f

∗

f^*

f∗.在实际的场景之中,我们遇到的参数肯定不止w,b。我们要寻找到到一个好的模型,使损失函数达到最小,则:

f

∗

=

arg

min

f

L

(

f

)

w

∗

,

b

∗

=

arg

min

w

,

b

L

(

w

,

b

)

=

arg

min

w

,

b

∑

n

=

1

10

(

y

^

n

−

(

b

+

w

⋅

x

c

p

n

)

)

2

\begin{aligned} f^{*}=\arg \min _{f} L(f) & \\ w^{*}, b^{*}=\arg \min _{w, b} L(w, b) & =\arg \min _{w, b} \sum_{n=1}^{10}\left(\hat{y}^{n}-\left(b+w \cdot x_{c p}^{n}\right)\right)^{2} \end{aligned}

f∗=argfminL(f)w∗,b∗=argw,bminL(w,b)=argw,bminn=1∑10(y^n−(b+w⋅xcpn))2

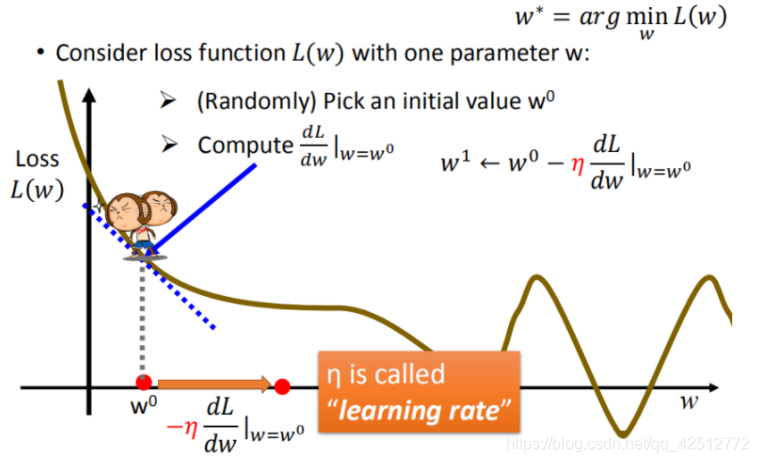

先从最简单的只有一个参数w入手,定义

w

∗

=

arg

min

w

,

b

L

(

w

)

w^{*} = \arg \min _{w, b} L(w)

w∗=argminw,bL(w),

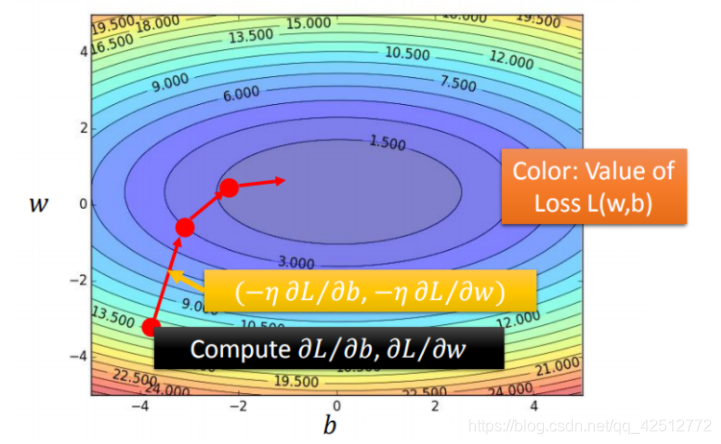

首先在这里引入一个概念 学习率 :移动的步长,如上图中

η

\eta

η

步骤1:随机选取一个

w

0

w^0

w0

步骤2:计算微分,也就是当前的斜率,根据斜率来判定移动的方向

大于0向右移动(增加w)

小于0向左移动(减少w)

步骤3:根据学习率移动

重复步骤2和步骤3,直到找到最低点

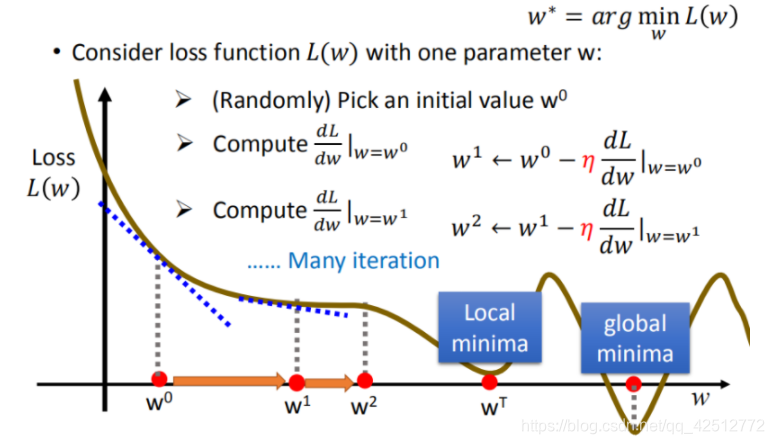

步骤1中,我们随机选取一个 w 0 w^0 w0 ,如上图所示,我们有可能会找到当前的最小值,并不是全局的最小值。

而对于两个变量时,一般的步骤如下图所示。

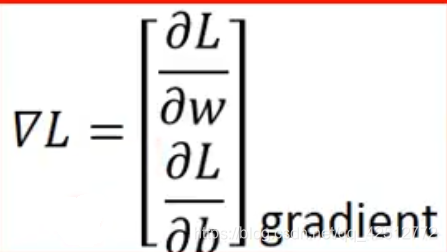

整理成一个更简洁的公式:

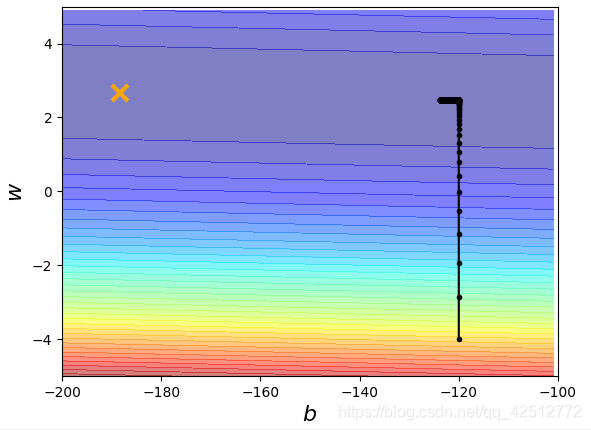

在梯度下降推演最优化的过程中,如果把w,b在图形中展示

每一条线围成的圈就是等高线,代表损失函数的值,颜色约深的区域代表的损失函数越小。红色的箭头代表等高线的法线方向。

四、如何验证训练模型的好坏

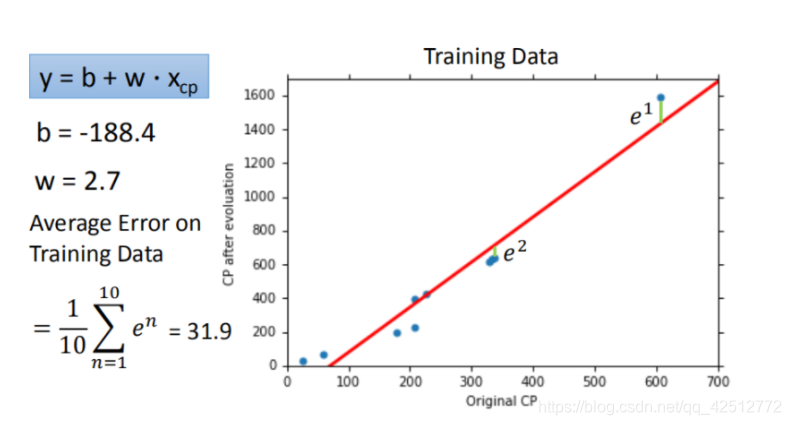

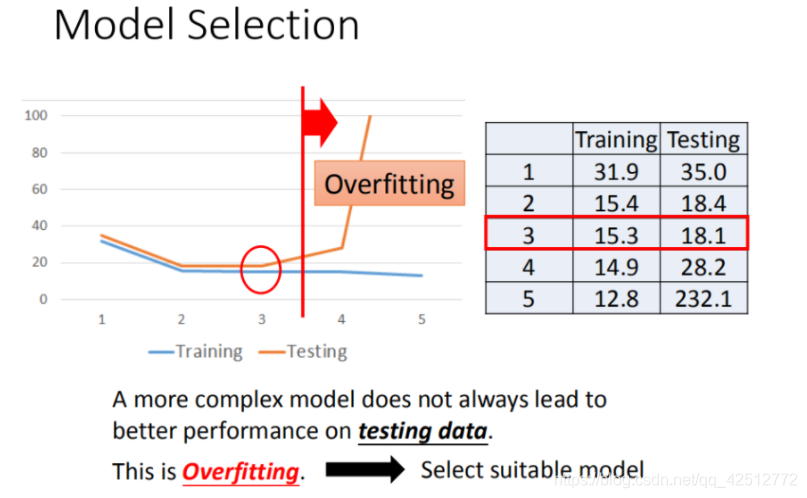

使用训练集和测试集的平均误差来验证模型的好坏 我们使用将10组原始数据,训练集求得平均误差为31.9,如图所示:

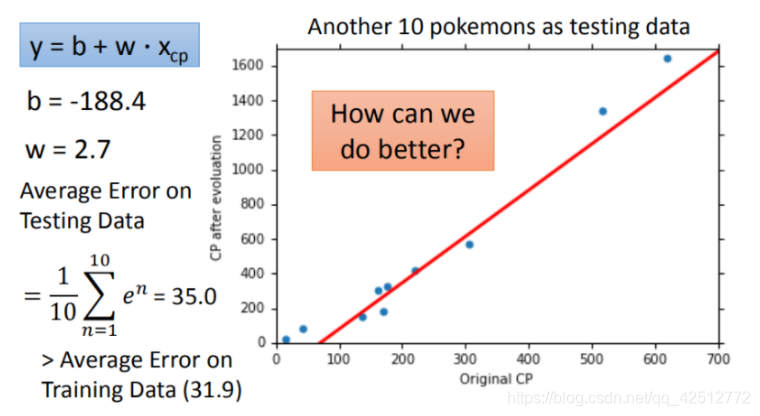

然后再使用10组Pokemons测试模型,测试集求得平均误差为35.0 如图所示:

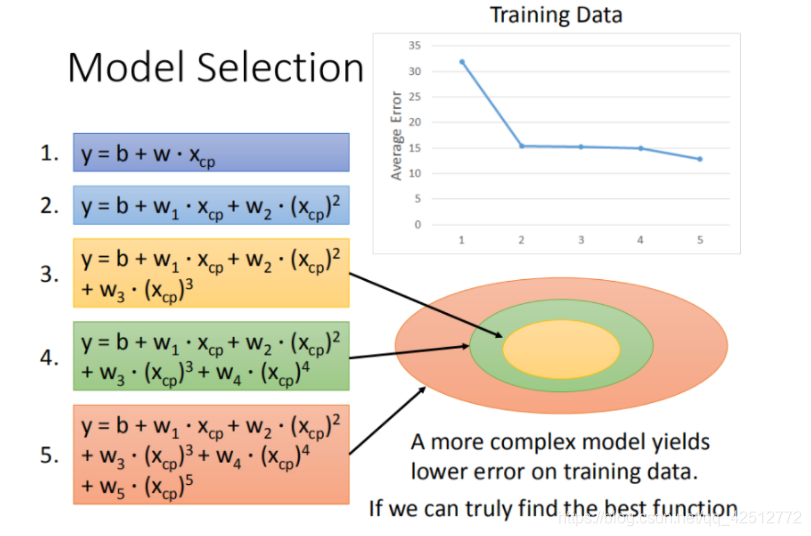

更强大复杂的模型:1元N次线性模型

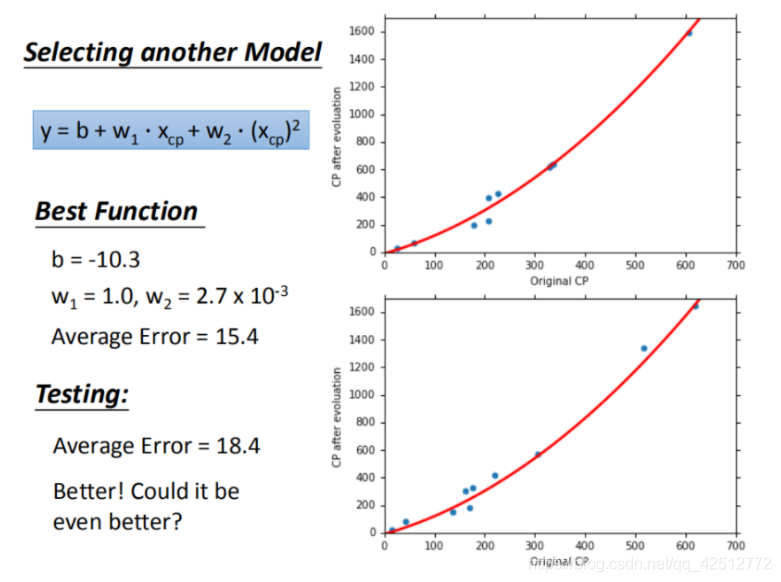

在模型上,我们还可以进一部优化,选择更复杂的模型,使用1元2次方程举例,如下图,发现训练集求得平均误差为15.4,测试集的平均误差为18.4。

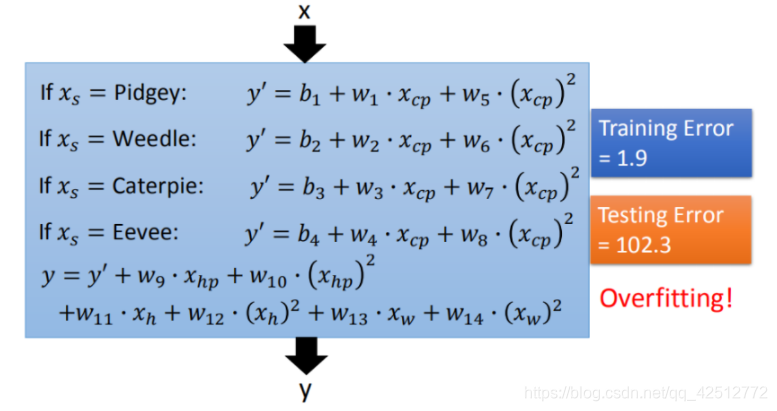

过拟合问题出现

在模型上,使用更高次方的模型进一步优化,但我们会发现在训练集上表现优秀的模型,到了测试集上效果反而变差了。这是因为模拟在训练集上出现了过拟合的问题。

将上述选择的模型所产生的错误率结果进行图形化展示,如下图所示,发现3次方以上的模型,出现了过拟合的现象。

五、步骤优化

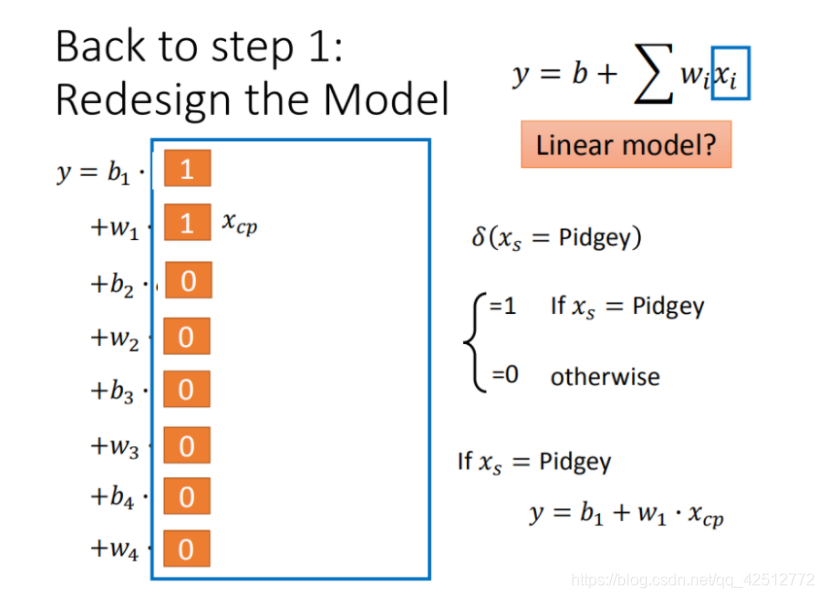

1、2个input的四个线性模型合并到一个线性模型中

2、使用更多的输入

将最开始分析得到的很多特征,都加入到模型当中

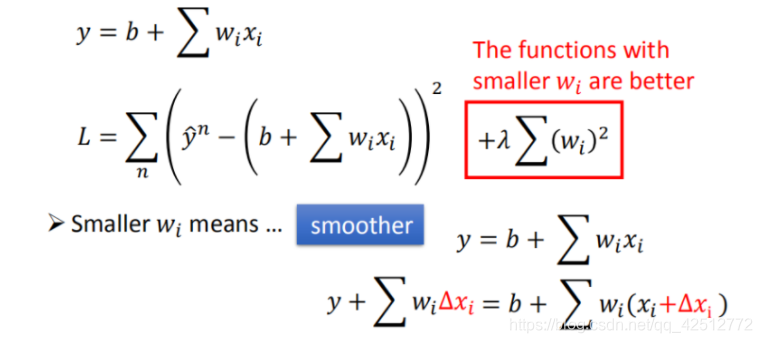

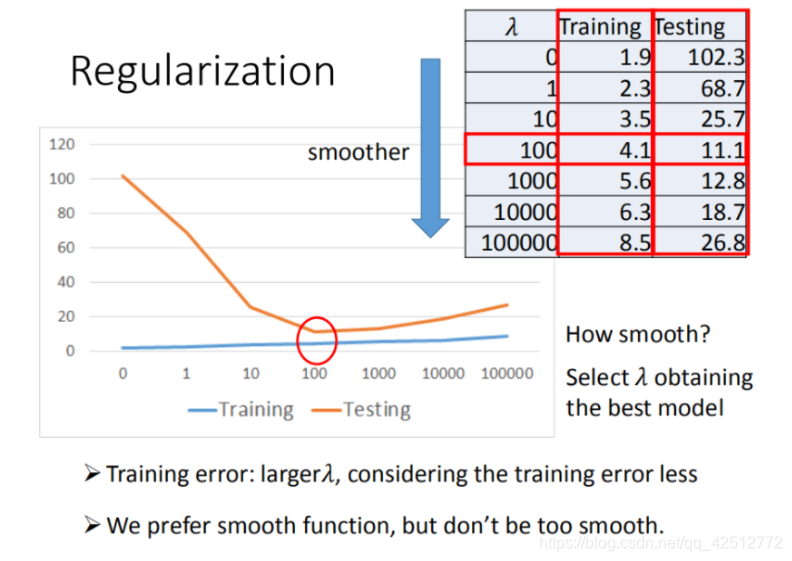

3、加入正则化

更多特征,但是权重 w 可能会使某些特征权值过高,仍旧导致过拟合现象,所以加入正则化。

w 越小,表示 functionfunction 较平滑的, functionfunction输出值与输入值相差不大。在很多应用场景中,并不是 w 越小模型越平滑越好,但是经验值告诉我们 w 越小大部分情况下都是好的。b 的值接近于0 ,对曲线平滑是没有影响。

六、代码实现

import numpy as np

import matplotlib.pyplot as plt

x_data = [338., 333., 328., 207., 226., 25., 179., 60., 208., 606.]

y_data = [640., 633., 619., 393., 428., 27., 193., 66., 226., 1591.]

x = np.arange(-200,-100,1)

y = np.arange(-5,5,0.1)

#损失函数

Z = np.zeros((len(x), len(y)))

for i in range(len(x)):

for j in range(len(y)):

b = x[i]

w = y[j]

Z[j][i] = 0

for n in range(len(x_data)):

Z[j][i] = Z[j][i] + (y_data[n] - b - w*x_data[n])**2

Z[j][i] = Z[j][i] / len(x_data)

def train(lr, iteration):

# 线性回归原始版

b = -120

w = -4

b_history = [b]

w_history = [w]

for i in range(iteration):

b_grad = 0.0

w_grad = 0.0

for n in range(len(x_data)):

b_grad = b_grad - 2.0 * (y_data[n] - b - w * x_data[n]) * 1.0

w_grad = w_grad - 2.0 * (y_data[n] - b - w * x_data[n]) * x_data[n]

# 更新参数

b -= lr * b_grad

w -= lr * w_grad

b_history.append(b)

w_history.append(w)

return b_history, w_history

#显示图像

def plot(b_history,w_history):

plt.contourf(x, y, Z, 50, alpha=0.5, cmap=plt.get_cmap('jet'))

plt.plot([-188.4], [2.67], 'x', ms=12, markeredgewidth=3, color='orange')

plt.plot(b_history, w_history, 'o-', ms=3, lw=1.5, color='black')

plt.xlim(-200, -100)

plt.ylim(-5, 5)

plt.xlabel(r'$b$', fontsize=16)

plt.ylabel(r'$w$', fontsize=16)

plt.show()

#原始调用lr=0.0000001

iteration = 100000

lr = 0.0000001

b_history,w_history=train(lr,iteration)

plot(b_history,w_history)

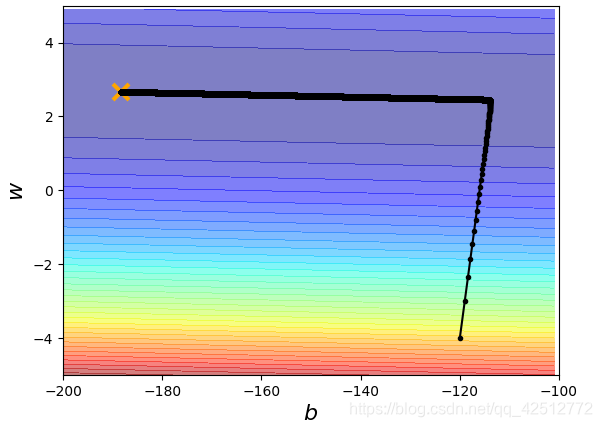

显示结果为:

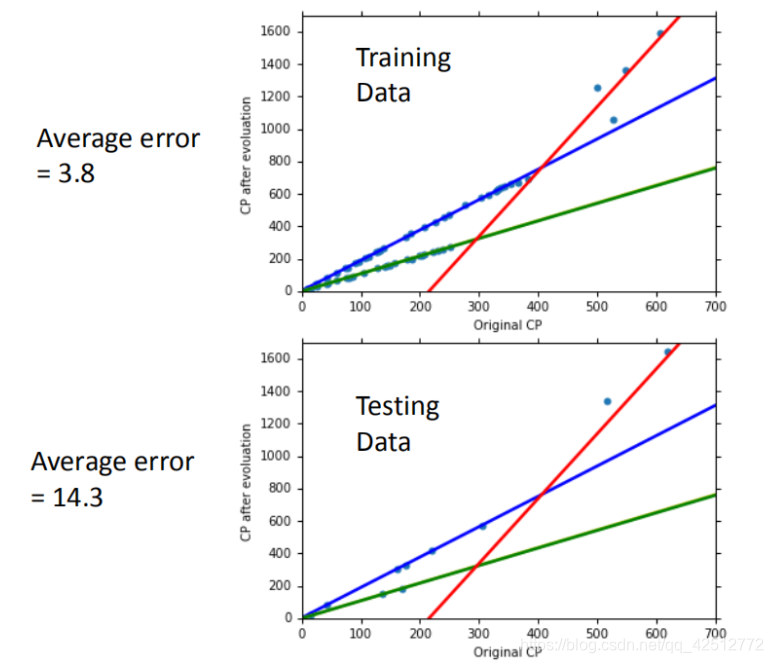

我们发现,在最终得到的结果中,最终回归得到的值离最终的理想状态值相差很大,因此需要调整参数,以达到最终回归出来的值尽可能接近理想值。

x_data = [338., 333., 328., 207., 226., 25., 179., 60., 208., 606.]

y_data = [640., 633., 619., 393., 428., 27., 193., 66., 226., 1591.]

x = np.arange(-200,-100,1)

y = np.arange(-5,5,0.1)

#损失函数

Z = np.zeros((len(x), len(y)))

for i in range(len(x)):

for j in range(len(y)):

b = x[i]

w = y[j]

Z[j][i] = 0

for n in range(len(x_data)):

Z[j][i] = Z[j][i] + (y_data[n] - b - w*x_data[n])**2

Z[j][i] = Z[j][i] / len(x_data)

def train(lr, iteration):

# 线性回归原始版

b = -120

w = -4

b_history = [b]

w_history = [w]

lr_b = 0

lr_w = 0

for i in range(iteration):

b_grad = 0.0

w_grad = 0.0

for n in range(len(x_data)):

b_grad = b_grad - 2.0 * (y_data[n] - b - w * x_data[n]) * 1.0

w_grad = w_grad - 2.0 * (y_data[n] - b - w * x_data[n]) * x_data[n]

lr_b = lr_b + b_grad ** 2

lr_w = lr_w + w_grad ** 2

# 更新参数

b -= lr / np.sqrt(lr_b) * b_grad

w -= lr / np.sqrt(lr_w) * w_grad

b_history.append(b)

w_history.append(w)

return b_history, w_history

#显示图像

def plot(b_history,w_history):

plt.contourf(x, y, Z, 50, alpha=0.5, cmap=plt.get_cmap('jet'))

plt.plot([-188.4], [2.67], 'x', ms=12, markeredgewidth=3, color='orange')

plt.plot(b_history, w_history, 'o-', ms=3, lw=1.5, color='black')

plt.xlim(-200, -100)

plt.ylim(-5, 5)

plt.xlabel(r'$b$', fontsize=16)

plt.ylabel(r'$w$', fontsize=16)

plt.show()

#原始调用lr=0.0000001

iteration = 100000

lr = 1

b_history,w_history=train(lr,iteration)

plot(b_history,w_history)

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言