智能股票分析预测系统是一个基于机器学习的股票分析与预测平台,集成了数据获取、特征工程、模型训练和可视化分析等功能。系统通过多种机器学习算法对股票历史数据进行分析,预测未来走势,并提供直观的可视化图表展示分析结果。

项目结构

- 📁 IntelligentStockAnalysisSystem/

- 📄 data_fetcher.py # 股票数据获取模块

- 📄 data_processor.py # 数据处理与特征工程

- 📄 feature_selector.py # 特征选择模块

- 📄 app.py # 程序入口

- 📄 model_trainer.py # 模型训练与评估

- 📄 visualizer.py # 可视化图表生成

- 📁 templates/ # HTML模板

- 📄 dashboard.html # 主仪表盘页面

- 📄 error.html # 错误页面

- 📁 static/ # 静态资源(CSS/JS/图片)

- 📄 README.md # 项目说明文档

功能特性

- 数据源支持:通过AKShare获取实时股票数据

- 高级特征工程:计算20+技术指标(MA、RSI、MACD、波动率等)

- 集成机器学习模型:随机森林、XGBoost、Lasso回归

- 时间序列验证:时间序列交叉验证

- 特征选择:基于相关性的特征筛选

- 可视化图表:生成8种专业分析图表

- 响应式Web界面:适配各种设备尺寸

快速开始

环境要求

- Python 3.8+

安装步骤

- 安装依赖

pip install flask akshare pandas numpy scikit-learn xgboost matplotlib seaborn

- 运行项目

python app.py

在实现项目核心功能时,可以按照项目的运行流程来逐步实现对应的模块功能,其主要流程如图所示:

![]()

一、项目构建

开发项目前,需要完成项目初始化的设置,主要是项目运行所需的一些依赖库的安装。诸如,Flask、AkShare、Pandas、Scikit-learnFlask等。进行依赖的安装时,可以通过pip命令进行统一的安装。

# 统一安装项目运行所需的依赖

pip install flask akshare pandas numpy scikit-learn xgboost matplotlib seaborn

1.数据采集

股票数据采集函数完整的实现代码如下所示:

def get_stock_data(stock_code="600519", start_date="20000101", end_date=None):

"""

获取股票历史数据

"""

if end_date is None:

# 默认结束日期为今天

end_date = datetime.now().strftime("%Y%m%d")

try:

df = ak.stock_zh_a_hist(

symbol=stock_code,

period="daily",

start_date=start_date,

end_date=end_date,

adjust="qfq"

)

# 如果数据为空,尝试其他数据源(并对备选数据源中的数据进行处理,使其列名与结构与主数据保持一致)

if df.empty:

df = ak.stock_zh_a_daily(symbol=stock_code, adjust="qfq")

df = df.reset_index()

df = df.rename(columns={'date': '日期', 'open': '开盘', 'close': '收盘',

'high': '最高', 'low': '最低', 'volume': '成交量'})

df = df[['日期', '开盘', '收盘', '最高', '最低', '成交量']]

return df

except Exception as e:

print(f"获取数据失败: {e}")

# 尝试备选数据源

try:

df = ak.stock_zh_a_daily(symbol=stock_code, adjust="qfq")

df = df.reset_index()

df = df.rename(columns={'date': '日期', 'open': '开盘', 'close': '收盘',

'high': '最高', 'low': '最低', 'volume': '成交量'})

df = df[['日期', '开盘', '收盘', '最高', '最低', '成交量']]

return df

except:

# 返回空DataFrame

return pd.DataFrame()

调用get_stock_data()函数,测试是否能正常获取股票数据,测试代码如下所示:

if __name__ == "__main__":

code="600519"

start_date="20000101"

# 获取股票数据

stock_data = get_stock_data(stock_code=code, start_date=start_date)

print(stock_data)

运行效果如下所示:

日期 股票代码 开盘 收盘 ... 振幅 涨跌幅 涨跌额 换手率

0 2020-01-02 600519 920.72 922.72 ... 2.98 -5.43 -53.00 1.18

1 2020-01-03 600519 909.72 871.28 ... 4.35 -5.57 -51.44 1.04

2 2020-01-06 600519 863.58 870.71 ... 2.94 -0.07 -0.57 0.50

3 2020-01-07 600519 870.22 887.25 ... 2.60 1.90 16.54 0.38

4 2020-01-08 600519 877.77 880.86 ... 1.46 -0.72 -6.39 0.20

... ... ... ... ... ... ... ... ... ...

1329 2025-07-01 600519 1409.00 1405.10 ... 0.61 -0.31 -4.42 0.16

1330 2025-07-02 600519 1409.50 1409.60 ... 1.05 0.32 4.50 0.21

1331 2025-07-03 600519 1412.00 1415.60 ... 1.04 0.43 6.00 0.19

1332 2025-07-04 600519 1415.70 1422.22 ... 1.55 0.47 6.62 0.23

1333 2025-07-07 600519 1422.28 1410.70 ... 0.95 -0.81 -11.52 0.19

[1334 rows x 12 columns]

2.数据处理与特征工程

import pandas as pd

import numpy as np

def process_data(df, prediction_window=5):

"""数据清洗与特征工程"""

# 重命名列

df = df.rename(columns={

'日期': 'date',

'开盘': 'open',

'收盘': 'close',

'最高': 'high',

'最低': 'low',

'成交量': 'volume'

})

# 转换日期类型并设置索引

df['date'] = pd.to_datetime(df['date'])

df.set_index('date', inplace=True)

# 添加基本技术指标

df['ma5'] = df['close'].rolling(5, min_periods=1).mean()

df['ma20'] = df['close'].rolling(20, min_periods=1).mean()

df['ma60'] = df['close'].rolling(60, min_periods=1).mean()

# 添加波动率指标

df['daily_return'] = df['close'].pct_change()

df['volatility_5d'] = df['daily_return'].rolling(5).std() * np.sqrt(252)

df['volatility_20d'] = df['daily_return'].rolling(20).std() * np.sqrt(252)

# 添加RSI和MACD

df['rsi'] = compute_rsi(df['close'])

df['macd'], df['signal'] = compute_macd(df['close'])

# 添加成交量相关指标

df['volume_ma5'] = df['volume'].rolling(5).mean()

df['volume_ma20'] = df['volume'].rolling(20).mean()

df['volume_ratio'] = df['volume'] / df['volume_ma20']

# 添加时间特征

df['year'] = df.index.year

df['month'] = df.index.month

df['day_of_week'] = df.index.dayofweek

df['day_of_month'] = df.index.day

# 添加滞后特征 计算当前时刻与过去 lag 天之间的收益率

for lag in [1, 2, 3, 5, 10]:

df[f'return_lag{lag}'] = df['close'].pct_change(lag)

# 修改目标变量计算(未来几天的收益率) -计算当前时刻与未来 prediction_window 天之后的收盘价之间的收益率

future_returns = df['close'].pct_change(prediction_window).shift(-prediction_window)

# 使用滚动平均平滑目标变量

smoothed_returns = future_returns.rolling(5, min_periods=1).mean()

# 添加滞后特征作为目标变量

df['future_return'] = smoothed_returns

# 添加方向目标变量(用于分类)

df['future_direction'] = np.where(df['future_return'] > 0, 1, 0)

# 清理无效数据

df.replace([np.inf, -np.inf], np.nan, inplace=True)

df.dropna(inplace=True)

# 验证数据

validate_data(df)

return df

def validate_data(df):

"""验证数据是否包含无效值"""

# 首先检查空值

if df.isnull().any().any():

print(f"警告: 数据包含 {df.isnull().sum().sum()} 个空值")

df.dropna(inplace=True)

# 只检查数值列中的无穷值

numeric_cols = df.select_dtypes(include=[np.number]).columns

for col in numeric_cols:

# 检查无穷值

if np.isinf(df[col]).any():

print(f"警告: 列 '{col}' 包含无穷值")

# 替换无穷值为NaN

df[col] = df[col].replace([np.inf, -np.inf], np.nan)

# 再次检查空值(替换无穷值后可能产生新的空值)

if df.isnull().any().any():

print(f"警告: 数据替换后包含 {df.isnull().sum().sum()} 个空值")

df.dropna(inplace=True)

# 检查异常大值

for col in numeric_cols:

if (df[col].abs() > 1e10).any():

print(f"警告: 列 '{col}' 包含异常大的数值")

return df

3.MACD指标与RSI指标函数完整的实现代码如下所示:

def compute_rsi(series, period=14):

"""计算相对强弱指数RSI(添加边界条件处理)"""

delta = series.diff()

gain = delta.where(delta > 0, 0)

loss = -delta.where(delta < 0, 0)

# 避免除零错误

avg_gain = gain.rolling(period, min_periods=1).mean()

avg_loss = loss.rolling(period, min_periods=1).mean()

# 添加额外保护:当avg_loss为0时直接返回100

rs = avg_gain / avg_loss

rs = np.where(avg_loss == 0, 100, rs) # 当损失为0时,RS设为100

rsi = 100 - (100 / (1 + rs))

# 替换无效值

rsi = pd.Series(rsi, index=series.index)

rsi = rsi.fillna(50) # 当数据不足时设为中性值50

rsi.replace([np.inf, -np.inf], 50, inplace=True)

return rsi

def compute_macd(series, fast=12, slow=26, signal=9):

"""计算MACD指标"""

ema_fast = series.ewm(span=fast, min_periods=1).mean()

ema_slow = series.ewm(span=slow, min_periods=1).mean()

macd = ema_fast - ema_slow

signal_line = macd.ewm(span=signal, min_periods=1).mean()

return macd, signal_line

4.关键特征的筛选

在前面股票特征的构建过程中,设置了许多的特征,例如收盘价均线(ma5、ma20、ma60等)、成交量均线(volume_ma5、volume_ma20等)、MACD指标、RSI指标等。但是在模型的训练预测阶段,并不是所有的特征都能产生作用,可能有些特征对最终的预测结果影响较大,而一些特征对最终的预测结果影响较小。因此为了提高模型的性能,需要对特征进行筛选,尽量选取一些对最终预测结果影响较大的特征。

def select_features(df):

"""选择相关性高的特征"""

# 计算特征与目标的相关性

corr_matrix = df.corr()

target_corr = corr_matrix['future_return'].abs().sort_values(ascending=False)

# 选择相关性大于0.05的特征

selected_features = target_corr[target_corr > 0.05].index.tolist()

# 确保包含关键特征

essential_features = [

'close', 'volatility_20d', 'rsi', 'macd', 'volume_ratio',

'year', 'ma5', 'ma20', 'daily_return', 'volume_ma5'

]

for feat in essential_features:

if feat not in selected_features and feat in df.columns:

selected_features.append(feat)

# 如果目标变量存在于筛选出的特征中移除目标变量

if 'future_return' in selected_features:

selected_features.remove('future_return')

if 'future_direction' in selected_features:

selected_features.remove('future_direction')

return selected_features

5.模型的构建与训练

构建了随机森林、XGBoost和Lasso三种模型进行训练,并对它们的性能进行评估,从中确定性能最好的模型。

def train_and_evaluate_models(X, y):

"""训练多个模型并评估性能"""

# 时间序列交叉验证

tscv = TimeSeriesSplit(n_splits=5)

# 构建模型字典

models = {

'RandomForest': RandomForestRegressor(

n_estimators=200,

max_depth=8,

min_samples_leaf=15,

max_features=0.7,

random_state=42,

n_jobs=-1

),

'XGBoost': XGBRegressor(

n_estimators=300,

max_depth=5,

learning_rate=0.03,

subsample=0.7,

colsample_bytree=0.8,

random_state=42,

n_jobs=-1

),

'Lasso': LassoCV(cv=5, random_state=42, max_iter=10000)

}

#记录模型训练结果的字典

results = {

'model': [],

'train_score': [],

'test_score': [],

'mae': []

}

# 记录最佳模型及其得分

best_model = None

best_score = -np.inf

for model_name, model in models.items():

fold_scores = []

fold_mae = []

for train_index, test_index in tscv.split(X):

X_train, X_test = X.iloc[train_index], X.iloc[test_index]

y_train, y_test = y.iloc[train_index], y.iloc[test_index]

# 标准化 - 仅使用训练数据

scaler = RobustScaler()

X_train_scaled = scaler.fit_transform(X_train)

X_test_scaled = scaler.transform(X_test)

# 训练模型

model.fit(X_train_scaled, y_train)

# 评估模型

train_score = model.score(X_train_scaled, y_train)

test_score = model.score(X_test_scaled, y_test)

y_pred = model.predict(X_test_scaled)

mae = mean_absolute_error(y_test, y_pred)

fold_scores.append(test_score)

fold_mae.append(mae)

# 计算平均性能

avg_score = np.mean(fold_scores)

avg_mae = np.mean(fold_mae)

results['model'].append(model_name)

results['train_score'].append(train_score)

results['test_score'].append(avg_score)

results['mae'].append(avg_mae)

# 选择最佳模型

if avg_score > best_score:

best_score = avg_score

best_model = model

# 使用最近3年数据重新训练最佳模型

recent_data = X[X.index.year >= datetime.now().year - 3]

if not recent_data.empty:

y_recent = y.loc[recent_data.index]

scaler = RobustScaler()

X_recent_scaled = scaler.fit_transform(recent_data)

best_model.fit(X_recent_scaled, y_recent)

return best_model, pd.DataFrame(results)

6.分析结果可视化

使用Matplotlib将模型的分析结果数据绘制为图表的形式方便用户进行数据分析。

def create_visualizations(df, model_performance, feature_importance):

"""生成股票分析可视化图表(优化版)"""

# 第一部分:技术指标图表

fig1 = plt.figure(figsize=(18, 22), constrained_layout=True)

gs = fig1.add_gridspec(4, 2)

# 1. 价格走势图(添加支撑/阻力线)

ax1 = fig1.add_subplot(gs[0, 0])

ax1.plot(df.index, df['close'], label='收盘价', linewidth=1.5, color='#1f77b4')

ax1.plot(df.index, df['ma20'], label='20日均线', linestyle='--', color='#ff7f0e')

ax1.plot(df.index, df['ma60'], label='60日均线', linestyle='-.', color='#2ca02c')

# 添加支撑阻力线(示例逻辑,可根据实际需求调整)

support = df['close'].rolling(50).min().dropna()

resistance = df['close'].rolling(50).max().dropna()

ax1.plot(support.index, support, 'g:', alpha=0.7, label='支撑位')

ax1.plot(resistance.index, resistance, 'r:', alpha=0.7, label='阻力位')

ax1.set_title('股票价格走势与技术指标', fontsize=14, fontweight='bold')

ax1.set_xlabel('日期')

ax1.set_ylabel('价格')

ax1.legend(loc='best', fontsize=9)

ax1.grid(True, linestyle='--', alpha=0.3)

# 2. 成交量分析(添加颜色编码)

ax2 = fig1.add_subplot(gs[0, 1])

# 根据涨跌着色

colors = np.where(df['close'].diff() >= 0, 'g', 'r')

ax2.bar(df.index, df['volume'], color=colors, alpha=0.7, label='成交量')

ax2.plot(df.index, df['volume_ma20'], color='#9467bd', linewidth=2, label='20日平均成交量')

ax2.set_title('成交量分析', fontsize=14, fontweight='bold')

ax2.set_xlabel('日期')

ax2.set_ylabel('成交量')

ax2.legend(loc='best', fontsize=9)

ax2.grid(True, linestyle='--', alpha=0.3)

# 3. RSI指标(添加超买超卖区域)

ax3 = fig1.add_subplot(gs[1, 0])

ax3.plot(df.index, df['rsi'], label='RSI', color='#8c564b', linewidth=1.5)

ax3.axhline(70, color='red', linestyle='--', alpha=0.5)

ax3.axhline(30, color='green', linestyle='--', alpha=0.5)

ax3.fill_between(df.index, 70, 100, color='red', alpha=0.1, label='超买区')

ax3.fill_between(df.index, 0, 30, color='green', alpha=0.1, label='超卖区')

ax3.set_title('相对强弱指数 (RSI)', fontsize=14, fontweight='bold')

ax3.set_xlabel('日期')

ax3.set_ylabel('RSI')

ax3.set_ylim(0, 100)

ax3.legend(loc='best', fontsize=9)

ax3.grid(True, linestyle='--', alpha=0.3)

# 4. MACD指标(优化柱状图显示)

ax4 = fig1.add_subplot(gs[1, 1])

ax4.plot(df.index, df['macd'], label='MACD', color='#17becf', linewidth=1.5)

ax4.plot(df.index, df['signal'], label='信号线', color='#e377c2', linewidth=1.5)

# 使用更高效的bar绘制方法

diff = df['macd'] - df['signal']

ax4.bar(df.index, diff, color=np.where(diff > 0, '#2ca02c', '#d62728'), alpha=0.5, width=1)

ax4.set_title('MACD指标', fontsize=14, fontweight='bold')

ax4.set_xlabel('日期')

ax4.set_ylabel('MACD')

ax4.legend(loc='best', fontsize=9)

ax4.grid(True, linestyle='--', alpha=0.3)

# 5. 波动率分析(添加布林带)

ax5 = fig1.add_subplot(gs[2, 0])

ax5.plot(df.index, df['volatility_20d'] * 100, label='20日波动率', color='#bcbd22', linewidth=1.5)

ax5.set_title('波动率分析', fontsize=14, fontweight='bold')

ax5.set_xlabel('日期')

ax5.set_ylabel('波动率 (%)')

ax5.legend(loc='best', fontsize=9)

ax5.grid(True, linestyle='--', alpha=0.3)

# 6. 模型性能比较(添加具体数值标签)

ax6 = fig1.add_subplot(gs[2, 1])

bars = ax6.bar(model_performance['model'], model_performance['test_score'],

color=['#1f77b4', '#ff7f0e', '#2ca02c'])

ax6.set_title('模型性能比较 (测试集$R^2$得分)', fontsize=14, fontweight='bold')

ax6.set_ylabel('$R^2$得分')

ax6.grid(True, linestyle='--', alpha=0.3)

# 在柱状图上添加数值标签

for bar in bars:

height = bar.get_height()

ax6.annotate(f'{height:.3f}',

xy=(bar.get_x() + bar.get_width() / 2, height),

xytext=(0, 3), # 3 points vertical offset

textcoords="offset points",

ha='center', va='bottom', fontsize=9)

# 7. 特征重要性(优化显示)

ax7 = fig1.add_subplot(gs[3, 0])

top_features = feature_importance.head(10).sort_values(by='importance', ascending=True)

colors = plt.cm.viridis(np.linspace(0, 1, len(top_features)))

ax7.barh(top_features['feature'], top_features['importance'], color=colors)

ax7.set_title('Top 10特征重要性', fontsize=14, fontweight='bold')

ax7.set_xlabel('重要性')

ax7.grid(True, linestyle='--', alpha=0.3)

# 8. 预测与实际对比(添加回归线和R²)

ax8 = fig1.add_subplot(gs[3, 1])

ax8.scatter(df['future_return'], df['prediction'], alpha=0.5, color='#d62728', s=20)

# 添加回归线

slope, intercept = np.polyfit(df['future_return'], df['prediction'], 1)

regression_line = slope * df['future_return'] + intercept

ax8.plot(df['future_return'], regression_line, 'b-', linewidth=2, label=f'回归线 (斜率={slope:.2f})')

# 添加45度参考线

ax8.plot([df['future_return'].min(), df['future_return'].max()],

[df['future_return'].min(), df['future_return'].max()],

'r--', linewidth=1.5, label='理想线')

# 计算R²

r2 = r2_score(df['future_return'], df['prediction'])

ax8.annotate(f'$R^2$ = {r2:.3f}', xy=(0.05, 0.9), xycoords='axes fraction', fontsize=12)

ax8.set_xlabel('实际收益率')

ax8.set_ylabel('预测收益率')

ax8.set_title('预测 vs 实际', fontsize=14, fontweight='bold')

ax8.legend(loc='best', fontsize=9)

ax8.grid(True, linestyle='--', alpha=0.3)

# 保存为Base64编码

buffer1 = BytesIO()

fig1.savefig(buffer1, format='png', dpi=120, bbox_inches='tight')

buffer1.seek(0)

img_base64 = base64.b64encode(buffer1.read()).decode()

plt.close(fig1) # 明确关闭图形释放内存

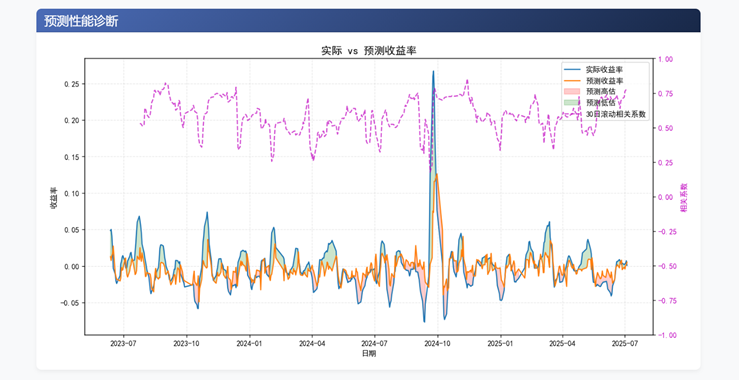

# 第二部分:诊断图 - 实际vs预测的时间序列对比

fig2, ax = plt.subplots(figsize=(12, 6), tight_layout=True)

# 绘制实际和预测值

ax.plot(df.index, df['future_return'], label='实际收益率', color='#1f77b4', linewidth=1.5)

ax.plot(df.index, df['prediction'], label='预测收益率', color='#ff7f0e', linewidth=1.5)

# 添加残差区域

ax.fill_between(df.index, df['future_return'], df['prediction'],

where=(df['prediction'] > df['future_return']),

color='red', alpha=0.2, label='预测高估')

ax.fill_between(df.index, df['future_return'], df['prediction'],

where=(df['prediction'] <= df['future_return']),

color='green', alpha=0.2, label='预测低估')

# 添加滚动相关系数

rolling_corr = df['future_return'].rolling(30).corr(df['prediction'])

ax2 = ax.twinx()

ax2.plot(df.index, rolling_corr, 'm--', alpha=0.7, label='30日滚动相关系数')

ax2.set_ylabel('相关系数', color='m')

ax2.tick_params(axis='y', labelcolor='m')

ax2.set_ylim(-1, 1)

ax.set_title('实际 vs 预测收益率', fontsize=14, fontweight='bold')

ax.set_xlabel('日期')

ax.set_ylabel('收益率')

# 合并图例

lines, labels = ax.get_legend_handles_labels()

lines2, labels2 = ax2.get_legend_handles_labels()

ax.legend(lines + lines2, labels + labels2, loc='best')

ax.grid(True, linestyle='--', alpha=0.3)

# 保存为Base64编码

buffer2 = BytesIO()

fig2.savefig(buffer2, format='png', dpi=120, bbox_inches='tight')

buffer2.seek(0)

diag_img = base64.b64encode(buffer2.read()).decode()

plt.close(fig2) # 明确关闭图形释放内存

return img_base64, diag_img

7.web交互

为了给用户提供一个良好的交互体验,我们可以借助Flask框架快速构建一个后端服务器,用来监听用户请求,并调用业务代码完成股票数据的查询、处理、模型性训练以及数据分析的完整流程,最终将分析结果返回到前端HTML页面中,实现前后端数据的交互。

from flask import Flask, render_template, request

import traceback

from datetime import datetime

from data_fetcher import get_stock_data

from data_processor import process_data

from feature_selector import select_features

from model_trainer import train_and_evaluate_models, get_feature_importance

from visualizer import create_visualizations

from sklearn.preprocessing import RobustScaler

# 实例化一个Flask框架应用

app = Flask(__name__)

@app.route('/', methods=['GET', 'POST'])

def stock_analysis():

print("表单提交内容:", request.form)

if request.method == 'POST':

stock_code = request.form.get('stock_code', '600519')

start_date = request.form.get('start_date', '20200101')

prediction_window = int(request.form.get('prediction_window', '5'))

else:

stock_code = "600519"

start_date = "20200101"

prediction_window = 5

print(start_date,'开始时间')

# 默认结束日期为今天

end_date = datetime.now().strftime("%Y%m%d")

if start_date >= end_date:

return render_template("error.html", message="起始日期不能大于等于结束日期")

try:

# 获取并处理数据

df = get_stock_data(stock_code, start_date=start_date,end_date=end_date)

if df.empty:

return render_template('error.html', message="无法获取股票数据,请检查股票代码是否正确")

# 构建特征

processed_df = process_data(df, prediction_window)

# 特征选择

features = select_features(processed_df)

X = processed_df[features]

y = processed_df['future_return']

# 训练模型并评估

model, model_performance = train_and_evaluate_models(X, y)

# 在完整数据集上生成预测

scaler = RobustScaler()

X_scaled = scaler.fit_transform(X)

processed_df['prediction'] = model.predict(X_scaled)

# 获取特征重要性

feature_imp = get_feature_importance(model, features)

# 关键指标计算

latest = processed_df.iloc[-1]

metrics = {

"股票代码": stock_code,

"当前价格": f"{latest['close']:.2f}",

"20日波动率": f"{latest['volatility_20d'] * 100:.2f}%",

"RSI指标": f"{latest['rsi']:.2f}",

"MACD信号": "看涨" if latest['macd'] > latest['signal'] else "看跌",

f"未来{prediction_window}日预期收益": f"{latest['prediction'] * 100:.2f}%",

"最佳模型": model_performance.loc[model_performance['test_score'].idxmax(), 'model'],

"模型测试得分": f"{model_performance['test_score'].max():.3f}"

}

# 模型性能表格

model_table = model_performance.to_dict('records')

# 特征重要性表格

feature_table = feature_imp.head(10).to_dict('records')

# 生成可视化图表

plot_img, diag_img = create_visualizations(processed_df.tail(500), model_performance, feature_imp)

# 获取股票名称

try:

import akshare as ak

stock_info = ak.stock_individual_info_em(symbol=stock_code)

stock_name = stock_info.loc[stock_info['item'] == '股票简称', 'value'].values[0]

print(stock_name)

except:

stock_name = "未知股票"

# 返回股票分析HTML页面,并将数据嵌入页面中

return render_template('dashboard.html',

plot=plot_img,# 股票分析与预测股票图片

diag_plot=diag_img,# 股票预测性能诊断图片

metrics=metrics,# 股票分析指标

model_table=model_table,# 模型性能表格

feature_table=feature_table,# 特征重要性表格

stock_name=stock_name,# 股票名称

prediction_window=prediction_window,# 预测窗口

start_date=start_date,# 开始日期

current_date=end_date,# 当前日期

stock_code=stock_code)# 股票代码

except Exception as e:

error_trace = traceback.format_exc()

return render_template('error.html', message=str(e), trace=error_trace)

# 错误处理页面

@app.errorhandler(404)

def page_not_found(e):

return render_template('error.html', message="页面未找到"), 404

@app.errorhandler(500)

def internal_server_error(e):

error_trace = traceback.format_exc()

return render_template('error.html', message="服务器内部错误", trace=error_trace), 500

# 程序主入口,运行Flask框架

if __name__ == "__main__":

app.run(debug=True)

项目运行效果图:

5186

5186

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言