本文介绍了如何使用Matplotlib库中的fill_between函数在时间轴上填充特定区间,以增强VIX指数的可视化效果,并展示了如何仅根据时间间隔操作,而不局限于日期范围。通过实例演示了代码实现和参数调整技巧。

本文介绍了如何使用Matplotlib库中的fill_between函数在时间轴上填充特定区间,以增强VIX指数的可视化效果,并展示了如何仅根据时间间隔操作,而不局限于日期范围。通过实例演示了代码实现和参数调整技巧。

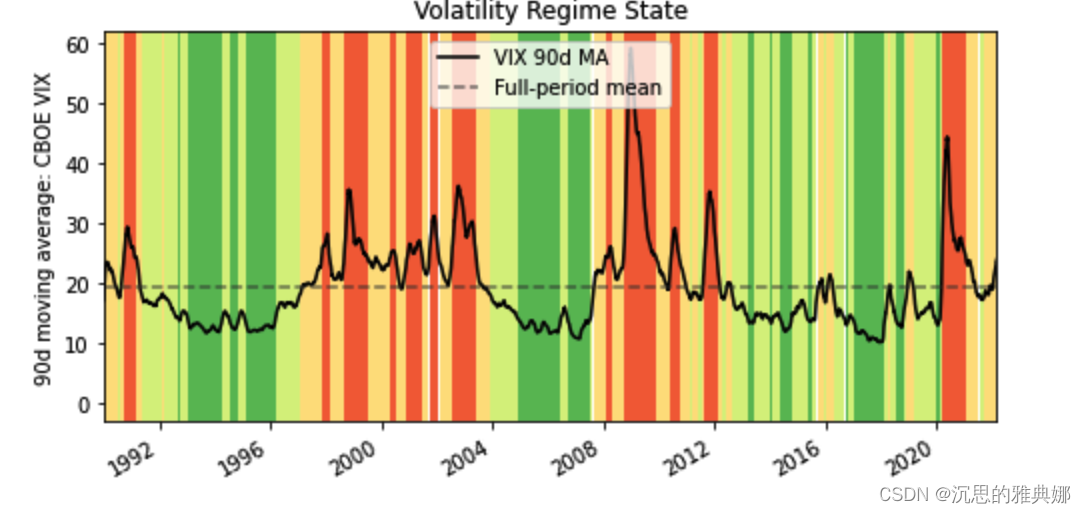

参考效果如下图:

上图实现代码如下:

import pandas as pd

import matplotlib.transforms as mtransforms

import matplotlib.pyplot as plt

url = 'https://fred.stlouisfed.org/graph/fredgraph.csv?id=VIXCLS'

vix = pd.read_csv(url, index_col=0, parse_dates=True, na_values='.',

infer_datetime_format=True,

squeeze=True).dropna()

cmap = plt.get_cmap('RdYlGn_r')

ma.plot(color='black', linewidth=1.5, marker='', figsize=(8, 4),

label='VIX 90d MA')

ax = plt.gca()

ax.set_xlabel('')

ax.set_ylabel('90d moving average: CBOE VIX')

ax.set_title('Volatility Regime State')

ax.grid(False)

ax.set_xlim(xmin=ma.index[0], xmax=ma.index[-1])

trans = mtransforms.blended_transform_factory(ax.transData, ax.transAxes)

for i, color in enumerate(cmap([0.2, 0.4, 0.6, 0.8])):

ax.fill_between(ma.index, 0, 1, where=state==i,

最低0.47元/天 解锁文章

最低0.47元/天 解锁文章

3万+

3万+

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言